29 Survey and Response Quality

Survey research generates a substantial fraction of the empirical record in the social, marketing, and health sciences. The credibility of that record rests on a chain of assumptions about what survey responses are: that the instrument measures what it is supposed to measure (validity); that repeated measurement returns the same answer (reliability); that respondents read, understand, and answer items the way the analyst intends (cognitive fidelity); that the realised sample is informative about the target population (representativeness); and that the response process is not contaminated by social-desirability, mode, interviewer, fatigue, or other systematic distortions. Each link in the chain is fragile in characteristic ways, and survey methodology as a discipline has spent six decades cataloguing and partially mitigating those fragilities.

This chapter is a synthesis of that body of work, with two unifying themes. The first is a taxonomy of the threats to survey-and-response quality, organised by where in the cognitive-and-mechanical pipeline they enter. The second is a response-side variance decomposition that goes one step beyond the classical reliability framework: a non-trivial share of the variance routinely labelled “measurement error” is not error in the conventional sense; it is intrinsic stochasticity in the response process itself, the same kind of irreducible noise that biology, neuroimaging, and physics have long acknowledged in their measurement models. Acknowledging this changes how we measure reliability, how we filter respondents, how we model decision making, and how we report results.

We treat both themes seriously. The chapter is not exclusively about intrinsic stochasticity, nor is it a generic survey-methodology textbook. It is a working manual for the analyst who must design, administer, and analyse a survey instrument with full awareness of where the threats to its credibility live and what the modern toolkit can do about each.

The treatment here builds on six bodies of literature. (1) Validity theory, beginning with Cronbach and Meehl (1955)’s construct-validity framework and Campbell and Fiske (1959)’s multitrait-multimethod matrix, which together define what it means for an instrument to measure what it claims to measure. (2) Cognitive psychology of survey response (Tourangeau et al. 2000; Schwarz 1999; Krosnick 1991, 1999; Schaeffer and Dykema 2020), which decomposes the response process into a sequence of cognitive operations and identifies error sources at each stage. (3) Classical psychometric reliability theory (Lord and Novick 1968; Cronbach 1951; Heise 1969; Wiley and Wiley 1970; Alwin 2007), which provides the test-retest, internal-consistency, and quasi-Markov simplex tools that have served the field for half a century. (4) Response-style and satisficing literature (Krosnick 1991; Greenleaf 1992; Baumgartner and Steenkamp 2001; Van Vaerenbergh and Thomas 2013; Zhang and Conrad 2014; Krosnick et al. 2002), which catalogs systematic non-substantive response patterns (acquiescence, extremity, midpoint, straightlining, speeding, no-opinion gaming) and the design choices that mitigate each. (5) The modern survey-methodology synthesis embodied in the Total Survey Error framework and adjacent practitioner references (Groves et al. 2009; Saris and Gallhofer 2014; Beatty and Willis 2007; Willis 2005; Schaeffer et al. 2010; Heerwegh 2009; Holbrook et al. 2003; Stantcheva 2023). (6) The decision-theoretic and behavioural-economic literature on probability matching (Vulkan 2000; Erev and Roth 1998; Lo et al. 2021; Kahneman and Tversky 1979), which provides a mechanistic explanation for the residual instability that the classical psychometric framework attributes to error. Recent work in survey methodology connects these threads and quantifies response instability under tight identifying assumptions (Clayton et al. 2025; Jenke and King 2026); the careless-responding literature (Meade and Craig 2012; Curran 2016; Oppenheimer et al. 2009; Berinsky et al. 2014; Hauser and Schwarz 2016; Aronow et al. 2019; Chandler et al. 2014) then converts the framework into practical filter design.

Roadmap. Section 29.1 introduces the four-stage cognitive model of how respondents answer a survey question and identifies where error and noise enter at each stage. Section 29.2 reviews the Total Survey Error framework and locates the contribution of this chapter within it. Section 29.3 treats validity as a separate concern from reliability: construct, convergent, discriminant, and predictive validity, with the Campbell and Fiske (1959) multitrait-multimethod matrix as the central operationalisation. Section 29.4 gives the modern taxonomy of response styles (acquiescence, extreme, midpoint, straightlining, speeding, no-opinion gaming, random responding) drawing on Krosnick (1991), Greenleaf (1992), Baumgartner and Steenkamp (2001), Van Vaerenbergh and Thomas (2013), Zhang and Conrad (2014), and Krosnick et al. (2002). Section 29.5 covers mode effects, interviewer effects, and cognitive interviewing as the standard pretest (Holbrook et al. 2003; Heerwegh 2009; Schaeffer et al. 2010; Schaeffer and Dykema 2020; Beatty and Willis 2007; Willis 2005). Section 29.6 defines instability formally and gives the estimator. Section 29.7 reviews classical reliability theory (Cronbach’s \(\alpha\), ICC, the Heise–Wiley simplex) and shows where it is silent on intrinsic stochasticity. Section 29.8 develops the three-way variance decomposition. Section 29.9 gives the decision-theoretic foundations. Sections 29.10–29.12 discuss what modulates stochasticity and how to filter it. Section 29.13 gives design recommendations; Section 29.14 gives analysis recommendations including a closed-form attenuation correction, a SIMEX procedure, and the modern conjoint audit (pAMCE, AMIE, satisficing, \(\bar D\) correction; Hainmueller et al. (2014), Egami and Imai (2019), Cuesta et al. (2022), Bansak et al. (2018), Clayton et al. (2025)). Section 29.15 gives a complete R workflow including production-ready straightlining, speeding, long-string, and Mahalanobis-based careless-responding detection. Sections 29.16–29.18 treat three advanced design and analysis topics that complement the within-session replication framework: anchoring vignettes for cross-cultural comparability (King et al. 2004; King and Wand 2007), sensitive-question methodology including randomised response, list experiments, and the Rosenfeld et al. (2016) empirical-validation benchmark (Warner 1965; Blair and Imai 2012; Bullock et al. 2011; Glynn 2013), and multilevel regression and poststratification (MRP) with deep interactions and dynamic IRT extensions (Park et al. 2004; Wang et al. 2015; Ghitza and Gelman 2013; Caughey and Warshaw 2015; Lax and Phillips 2009). Section 29.20 covers online-panel quality, non-naïveté, professional respondents, duplicate accounts, and bot detection (Chandler et al. 2014; Berinsky et al. 2012). Section 29.21 addresses synthetic respondents and large language models (Argyle et al. 2023; Bisbee et al. 2024). Section 29.19 covers the modern robustness, replicability, and fraud-detection toolkit (Simmons et al. 2011; Simonsohn, Leif D. Nelson, et al. 2014a; Simonsohn 2013; Simonsohn et al. 2020; Ioannidis 2005; Open Science Collaboration 2015; Camerer et al. 2018). The chapter closes with a short note on causal inference, a summary, a further-reading list, and exercises. For the broadest modern guide to designing original surveys, Stantcheva (2023) is the single best entry point.

29.1 The cognitive process of answering a survey question

The most influential synthesis of how respondents construct an answer to a survey question is the four-stage model of Tourangeau et al. (2000). The model decomposes the response process into

- Comprehension of the question.

- Retrieval of relevant information from memory.

- Judgment integrating retrieved information into a tentative answer.

- Response selection, mapping the judgment onto the available response options.

Each stage admits its own error sources. Figure 29.1 renders the four-stage pipeline as a flow diagram with the dominant error mechanism branching off each stage, and Table 29.1 gives the same content in tabular form for reference.

Figure 29.1: The four-stage cognitive model of survey response (Tourangeau, Rips and Rasinski 2000) as a flow diagram. The respondent’s answer flows through four sequential cognitive stages; the dominant error mechanism at each stage is shown as a branch.

| Stage | Cognitive operation | Dominant error mechanism |

|---|---|---|

| 1. Comprehension | Parse syntax; assign reference; infer pragmatic meaning | Question wording; vague terms; double-barrelled items |

| 2. Retrieval | Search memory for relevant beliefs, episodes, attitudes | Recall failure; availability; omission of relevant evidence |

| 3. Judgment | Integrate retrieved evidence into a tentative answer | Anchoring; framing; satisficing; mood-as-information |

| 4. Response selection | Map the answer onto the response options | Acquiescence; central tendency; extreme responding; scale interpretation |

Several points follow from Table 29.1 that recur throughout the chapter.

First, most instrument-side measurement-error work targets stages 1 and 4: clearer wording reduces comprehension error, better-calibrated response options reduce mapping error. The interior stages 2 and 3 are far less under instrument control.

Second, the optimizing–satisficing tradeoff (Krosnick 1991, 1999) sits at stage 3. A respondent has a finite cognitive budget; when the cost of fully retrieving and integrating evidence exceeds the perceived benefit, the respondent satisfices, generating an answer that is plausible but not optimal. Satisficing is the cognitive mechanism through which item complexity and respondent fatigue inflate response noise, and it is the mechanism we will repeatedly point to when explaining why intrinsic stochasticity has the empirical signature it does.

Third, probability matching at stage 4 (Section 29.9) is conceptually distinct from satisficing at stage 3 even though they are easy to confuse. Satisficing reflects effort allocation; probability matching reflects how an internal probabilistic judgment is converted into a choice. Both inflate \(\bar D\), but they imply different design responses.

The four-stage model is also the right place to locate the classical question-wording literature. Schwarz (1999) synthesises three decades of experimental evidence that subtle features of the stimulus (the verbal labels on a scale, the numeric range, the order of options, the prior questions) systematically shift the answer obtained. Two stylized findings illustrate the family. When respondents are asked how often they are “really irritated” with response options ranging from “less than once a year” to “more than once a month”, they report being irritated infrequently; when given options ranging from “less than once a day” to “several times a month”, they report being irritated more frequently. When response options for daily television viewing are centred on a middle option of two hours, respondents anchor low; when centred on four hours, they anchor high. These are not idiosyncratic anomalies; they are systematic effects of the response-option set acting on stages 1 and 4. The most extensive catalog of such effects in survey methodology remains Schuman and Presser (1981).

29.2 The Total Survey Error framework

The standard graduate-level synthesis of where error enters survey estimates is the Total Survey Error (TSE) framework of Groves et al. (2009). TSE partitions estimate error into the components in Table 29.2. The framework is the lingua franca for survey-methodology audits; locating this chapter’s contribution within it sharpens what is being claimed.

| Component | Source | Reducible by |

|---|---|---|

| Coverage error | Mismatch between the target population and the sampling frame | Better frame; multi-frame designs |

| Sampling error | Variation across samples of the same size from the same frame | Larger \(n\); design-based variance reduction (Chapter on Sampling) |

| Nonresponse error | Differences between respondents and non-respondents in the realised sample | Targeted follow-up; weighting adjustments |

| Measurement error (instrument) | Question wording, mode, interviewer, layout | Cognitive pretesting; mode harmonisation; question redesign |

| Measurement error (respondent) | Comprehension, retrieval, judgment, response selection | Better stage-1 and stage-4 design; but not stage-2/3 noise |

| Processing error | Coding, editing, weighting, imputation | Process audits; double coding |

Figure 29.2 renders the framework as a taxonomy tree, highlighting the respondent-side measurement-error branch where the contribution of this chapter is concentrated.

Figure 29.2: The Total Survey Error framework as a taxonomy tree. The respondent-side measurement-error branch (highlighted) is the focus of this chapter; the remaining branches are addressed in the chapters on Sampling, Imputation, Biases, and elsewhere.

The contribution of this chapter sits in the respondent-side branch of Figure 29.2 and Table 29.2: the share of measurement error attributable to the respondent’s own response-generation process. The argument is that this row is conventionally treated as a residual that better instrument design will eventually shrink, when in fact a substantial part of it has the structural properties of intrinsic stochasticity and cannot be designed away.

29.3 Validity: are we measuring what we think we are measuring?

Reliability and validity are conceptually distinct: a perfectly reliable instrument can measure the wrong thing, and a valid instrument can be noisy. Most of this chapter is about reliability and noise; this short section establishes the validity framework that the rest of the chapter assumes.

Cronbach and Meehl (1955) introduce the modern concept of construct validity as the central question of measurement: does the instrument measure the latent construct it claims to measure? They distinguish four types of validity, three of which remain core to the modern toolkit (Table 29.4).

| Type | Question | Standard test |

|---|---|---|

| Content validity | Do the items cover the full conceptual domain of the construct? | Expert review against a domain map |

| Criterion validity (concurrent) | Does the instrument correlate with a contemporaneous gold-standard measure? | Pearson/polychoric correlation with the criterion |

| Criterion validity (predictive) | Does the instrument predict a future outcome of theoretical interest? | Out-of-sample predictive performance |

| Construct validity; convergent | Do measures of the same construct correlate strongly? | Off-diagonal validity correlations in the MTMM matrix |

| Construct validity; discriminant | Do measures of distinct constructs correlate weakly? | Heterotrait correlations smaller than monotrait |

| Face validity | Does the instrument look sensible to respondents and reviewers? | Cognitive interviewing and pretest review |

| Known-groups validity | Does the instrument differ between groups known to differ on the construct? | Two-sample \(t\)-test or known-group SEM |

In the marketing-research tradition, the standard structural-equation operationalisation of construct validity is Bagozzi and Yi (1988), who codified a now-canonical checklist for SEM-based measurement-model evaluation: composite reliability, average variance extracted (AVE), \(\chi^2\) and incremental fit indices, and discriminant-validity tests via \(\sqrt{\mathrm{AVE}}\) versus inter-construct correlations. For a Springer marketing audience, Bagozzi and Yi is the entry point; the broader SEM machinery is covered in the chapter on Structural Equation Modeling.

The single most influential operationalisation of construct validity is the multitrait-multimethod (MTMM) matrix of Campbell and Fiske (1959). The MTMM matrix is the correlation matrix of \(T \times M\) measurements (each of \(T\) traits administered through each of \(M\) methods). Convergent validity is read off the monotrait-heteromethod diagonal: measures of the same trait through different methods should correlate strongly. Discriminant validity is read off the heterotrait-heteromethod off-diagonal: measures of different traits through different methods should correlate weakly. A trait that fails convergent validity is not measured by the instrument; a trait that fails discriminant validity is not distinguishable from neighbouring constructs. Saris and Gallhofer (2014) develops the modern structural-equation operationalisation of MTMM, including the MTMM-MTSM extension that simultaneously estimates trait, method, and unique variance.

A practical hierarchy for the analyst designing a new survey instrument is:

- Map the construct domain. Write down what the construct is and is not. Validate the domain map against an expert panel (content validity).

- Cognitively pretest the items against members of the target population (face validity, comprehension).

- Pilot the instrument alongside a gold-standard alternative if available (criterion validity).

- For multi-construct instruments, run an MTMM design if the budget allows (convergent and discriminant validity).

- Field the instrument and measure reliability (the rest of this chapter).

Order matters. Validity precedes reliability. A reliable measurement of the wrong construct is worse than no measurement at all, because it gives the analyst false confidence. The remainder of this chapter assumes the validity work has been done.

29.3.1 Measurement invariance

For comparisons across groups, time, or modes, validity requires more than within-group construct validity: the latent factor structure must hold equivalently across the comparison units. Vandenberg and Lance (2000) codify the measurement invariance hierarchy as a series of nested confirmatory-factor-analysis restrictions on (a) configural invariance (same factor structure), (b) metric invariance (equal factor loadings), (c) scalar invariance (equal item intercepts), and (d) strict invariance (equal item residual variances). Cross-group comparisons of latent means require at least metric and scalar invariance; comparisons of regression coefficients on the latent factor require at least metric invariance. The lavaan and semTools R packages implement the standard tests.

For survey research with cross-cultural or cross-mode comparisons, measurement invariance is the SEM-side counterpart of the anchoring-vignettes apparatus in Section 29.16: both diagnose differential item functioning, but invariance testing relies on parametric structural-equation assumptions whereas anchoring vignettes use a non-parametric calibration design.

29.3.2 Where the validity apparatus meets the rest of the chapter

The psychometric reliability apparatus described in Section 29.7 measures how consistently the instrument fires under repeated administration; the response-quality apparatus described in Sections 29.4–29.5 measures whether respondents are doing their part of the job seriously; and the intrinsic-stochasticity framework developed in Sections 29.6–29.9 addresses the irreducible component of within-respondent noise that survives the first two diagnostics.

29.4 Response styles, satisficing, and non-substantive responding

Even with a valid instrument and an attentive respondent, a substantial share of recorded variance reflects systematic non-substantive responding; patterns driven by the response process rather than the substantive content. The classical taxonomy (Krosnick 1991; Baumgartner and Steenkamp 2001; Van Vaerenbergh and Thomas 2013) distinguishes the patterns in Table 29.6.

| Style | Definition | Detection (single item) | Mitigating design |

|---|---|---|---|

| Acquiescence (ARS) | Tendency to agree regardless of content | Item-pair (positive vs. negated) agreement | Reverse-coded items; balanced scales |

| Disacquiescence (DARS) | Tendency to disagree regardless of content | Item-pair (positive vs. negated) disagreement | Reverse-coded items; balanced scales |

| Extreme response style (ERS) | Tendency to choose scale endpoints | Greenleaf (1992) ERS scale | Avoid 7+ point unanchored scales |

| Midpoint / central tendency (MRS) | Tendency to choose the scale midpoint | Frequency of midpoint responses | Even number of options forces non-midpoint |

| Net acquiescence (NARS) | ARS minus DARS in proportional terms | Composite of ARS and DARS | Balanced scales with reverse coding |

| Noncontingent / random responding | Random responses unrelated to item content | Mahalanobis distance; consistency indices | Cognitive pretest; remove items respondents cannot interpret |

| Straightlining | Same response across multiple grid items | Within-row variance in matrix questions | Vary item order; avoid long matrix grids |

| Speeding | Time on task below a content-comprehension floor | Within-respondent percentile of TOT | Burn-in TOT floor (Section 29.12) |

29.4.1 The optimizing–satisficing tradeoff

The mechanism unifying most of Table 29.6 is Krosnick (1991)’s satisficing model: the respondent allocates cognitive effort across stages of the four-stage cognitive model (Section 29.1) until perceived marginal benefit equals perceived marginal cost, then short-cuts the remaining stages. Strong satisficing truncates the response process at the comprehension stage and substitutes a heuristic answer (acquiescence, midpoint selection, straightlining); weak satisficing truncates the retrieval/judgment stages and substitutes a partial-evidence answer.

The key empirical regularity is that satisficing rises with item complexity, declines with respondent ability and motivation, and inflates as the survey gets longer. The implication is that the first third of a long instrument typically yields cleaner measurement than the last third, even on the same items.

29.4.2 Acquiescence, extremity, and midpoint

Baumgartner and Steenkamp (2001) provides the modern marketing-research operationalisation of the response-style taxonomy. Using consumer surveys from 11 EU countries, they document that:

- ARS, DARS, ERS, and MRS are systematic (within-respondent stable) and correlated (a respondent high on ARS is also typically high on ERS), implying a low-dimensional latent structure rather than independent quirks.

- Response styles bias scale scores by an amount that depends on (i) the proportion of reverse-coded items and (ii) the deviation of the scale mean from the response-scale midpoint.

- Cross-country comparisons of substantive scale scores can be substantially biased when response-style prevalence differs across cultures, even when the underlying construct does not.

The remedies follow naturally: include reverse-coded items to balance acquiescence-induced bias, use scales with even numbers of options to suppress midpoint choosing, and either (a) measure response styles via an auxiliary battery (Greenleaf 1992) and partial-out their variance, or (b) use IRT-based extreme-response-style estimation that recovers latent ERS as a second factor alongside the substantive trait.

29.4.3 Straightlining and speeding

In matrix-grid questions and long batteries of similar items, two of the most consequential patterns are straightlining (selecting the same response across all rows of a grid) and speeding (responding much faster than reasonable comprehension allows). Zhang and Conrad (2014) establish that the two are tightly coupled: respondents who speed on early items are dramatically more likely to straightline on later grid questions, and the speed-straightline coupling is strongest for less-educated respondents and for younger respondents.

Detection follows from two simple operationalisations. First, long-string \(L_i = \max_j \mathbb{1}\{X_{i,j} = X_{i,j-1}\}\) counts the longest consecutive identical response sequence within respondent \(i\); values above a sample-specific cutoff (typically the 95th percentile, or any value above \(0.7 \times K\) for a \(K\)-row grid) flag straightlining. Second, page-level speeding \(\mathrm{Speed}_i^{(p)} = \mathrm{TOT}_i^{(p)} / \overline{\mathrm{TOT}^{(p)}}\) flags respondents below \(0.5\) of the page-level median time. Section 29.15 provides production-ready code.

29.4.4 Don’t-know responses and item nonresponse

A separate component of non-substantive responding is the use of “don’t know” (DK) or “no opinion” response options when offered. Krosnick et al. (2002) provides the canonical empirical evaluation: contrary to the seasoned-survey-researcher intuition that offering DK reduces guessing by respondents who hold no true opinion, the data show that DK is preferentially selected by respondents low in cognitive skills, by respondents answering secretly rather than orally, and by respondents late in long surveys: the satisficing signature. Including DK options can therefore reduce the total information content of the instrument by inviting low-effort opt-out.

The recommendation that follows is design-conditional. Where the analyst has reason to believe a meaningful share of the population holds genuinely no opinion (low-salience policy items, novel constructs), offer DK and treat it as substantive. Where the analyst has reason to believe most of the population holds an opinion of some kind (well-known issues, well-anchored attitudes), omit DK and accept some forced-choice noise as the price of fewer satisficed responses.

29.4.5 Pure non-contingent responding

Beyond the structured patterns above, a small fraction of respondents simply respond at random. Mahalanobis distance \(D_i^2 = (\mathbf{x}_i - \bar{\mathbf{x}})^\top \mathbf{S}^{-1} (\mathbf{x}_i - \bar{\mathbf{x}})\) on the response vector flags multivariate outliers; person-total correlation \(r_i = \mathrm{cor}(\mathbf{x}_i, \bar{\mathbf{x}}_{-i})\) flags respondents whose answer pattern is uncorrelated with the sample-mean answer pattern. Meade and Craig (2012) recommend computing both alongside long-string and TOT diagnostics and using the joint distribution rather than any single index. Section 29.11.2 implements the joint detection battery.

29.5 Mode, interviewer, and pretesting effects

Survey mode and interviewer characteristics are not innocuous design choices. A mode change can shift the recorded response distribution by amounts comparable to substantive treatment effects in the same instrument; an interviewer-induced effect on a single sensitive item can dwarf the standard error of the population estimate.

29.5.1 Mode effects

Three large empirical literatures document mode effects. Holbrook et al. (2003) compare telephone with face-to-face interviewing on national probability samples with long questionnaires; telephone respondents satisfice more (more midpoint, more no-opinion, more straightlining) and exhibit larger social-desirability bias on sensitive items than face-to-face respondents in the same survey design. Heerwegh (2009) compares face-to-face and web administration of the same instrument with random assignment of mode within a single sample; the web condition reduces social-desirability bias on sensitive items at the cost of higher item nonresponse and shorter open-ended responses. The umbrella synthesis in Schaeffer and Dykema (2020) catalogues additional mode effects on response distribution shape, breakoff rates, and cognitive load.

The implication for analysis is direct: calibrate filter floors mode-by-mode, never pool. A TOT floor of 6 seconds that is sensible for a face-to-face conjoint item is too lax for the same item self-administered online and too strict for the same item asked over the phone with an interviewer reading the prompt aloud.

29.5.2 Interviewer effects

Where interviewers are present, an additional layer of design effect enters: interviewers vary in how they read prompts, probe responses, and code answers. Schaeffer et al. (2010) and Schaeffer and Dykema (2020) synthesise the standardised-interviewing literature. Two practical implications.

- Interviewer ID should be a level in any multilevel model of the survey response. Variance attributable to interviewers is rarely small; treating it as zero biases standard errors downward and inflates Type I error.

- Interviewer variance is a quality diagnostic. Large interviewer variance on a question that should admit a single objective answer (e.g., a factual recall item) suggests interviewer-introduced measurement error and motivates either re-training, item redesign, or both.

29.5.3 Cognitive interviewing as the standard pretest

Beatty and Willis (2007) synthesise the now-standard cognitive-interviewing protocol for pretesting survey items. The respondent is administered the draft item alongside a verbal protocol (think-aloud, scripted probes, retrospective debriefing) that surfaces comprehension, retrieval, and judgment problems. Willis (2005) develops the practitioner’s manual.

A workable cognitive-interview protocol for a new instrument is:

- Draft the items.

- Recruit 8–15 respondents broadly representative of the target population.

- Administer each draft item with a think-aloud or concurrent-probe verbal protocol.

- Code observed problems by stage of the four-stage model (comprehension, retrieval, judgment, response selection).

- Revise items where the same problem recurs in three or more interviews.

- Iterate.

Cognitive interviewing is a complement to, not a substitute for, larger-scale field pretesting. Behaviour coding (recording the frequency of interviewer probes, respondent requests for clarification, and breakoffs) on a field pretest catches design problems that cognitive interviewing misses, particularly in interviewer-administered modes (Schaeffer et al. 2010).

29.6 Defining survey instability

29.6.1 Setup and notation

Consider a finite population of \(N\) respondents and a binary survey item. Let \(C_{it} \in \{0, 1\}\) denote respondent \(i\)’s observed choice at administration \(t \in \{1, 2\}\), where the two administrations are separated by some elapsed time and possibly by intervening items. Define individual-level survey instability as the indicator

\[\begin{equation} D_i \;=\; \mathbb{1}\!\left( C_{i1} \neq C_{i2} \right), \tag{29.1} \end{equation}\]

and population mean instability is the average of \(D_i\) from equation (29.1) across the population,

\[\begin{equation} \Delta \;=\; \frac{1}{N} \sum_{i=1}^{N} D_i. \tag{29.2} \end{equation}\]

The complement \(1 - \Delta\) in equation (29.2) is sometimes called intra-respondent reliability on a binary item. It is conceptually distinct from inter-rater reliability (agreement across raters on the same target), internal consistency (Cronbach’s \(\alpha\), agreement across items in a scale; Section 29.7), and unidimensionality (whether the items load on a single latent factor). Intra-respondent reliability is the within-respondent within-item analogue.

For a sample of \(n < N\) respondents drawn under a sampling design with inclusion indicator \(S_i \in \{0,1\}\) and inclusion probability \(\pi_i^{\mathrm{(samp)}}\), the design-unbiased Horvitz–Thompson estimator of \(\Delta\) is

\[\begin{equation} \widehat{\Delta} \;=\; \frac{1}{N}\sum_{i=1}^{N} \frac{S_i\, D_i}{\pi_i^{\mathrm{(samp)}}}. \tag{29.3} \end{equation}\]

Under simple random sampling without replacement and ignorable nonresponse, equation (29.3) collapses to the sample mean \(\bar D = n^{-1} \sum_{i:S_i=1} D_i\). We use \(\bar D\) in the rest of the chapter; design-based corrections required when the sampling design departs from simple random are covered in the chapter on Sampling.

29.6.2 Identifying assumptions

For \(\bar D\) to estimate something we are willing to call instability rather than something else that happens to be a difference rate, three assumptions must hold.

Assumption 1 (No material change). Between the two administrations, no information has reached respondent \(i\) that would change the meaning of the question or the value of the response options. Formally, the respondent’s information set \(\mathcal{F}_i\) relevant to the item is the same at both administrations.

Assumption 2 (No memory). At administration \(t = 2\), respondent \(i\) has no recollection of having been asked the item at \(t = 1\). Were memory present, \(C_{i2}\) would be a function of \(C_{i1}\) rather than an independent draw from the response process.

Assumption 3 (Attrition at random). Whether respondent \(i\) is observed at both administrations is independent of \(D_i\), possibly conditional on observed covariates.

These three assumptions interact in ways that traditional panel surveys cannot satisfy simultaneously (Table 29.8).

| Design | A1 (no change) | A2 (no memory) | A3 (attrition at random) |

|---|---|---|---|

| Wide-spaced panel waves | Hard; world changes between waves | Easy; long interval | Hard; selective attrition |

| Narrow-spaced panel waves | Easier; short interval | Hard; recent question recalled | Easier; short interval |

| Within-session replication | Trivially holds (single session) | Holds with sufficient distractor items (Clayton et al. 2025) | Trivially holds (no inter-session attrition) |

The methodological move that allows clean estimation of \(\Delta\) is, accordingly, to ask the same item twice within a single survey session, separated by distractor items. Within-session replication satisfies Assumption 1 by construction, satisfies Assumption 3 because attrition is essentially absent within a session, and satisfies Assumption 2 if the distractor block is sufficient; in the Clayton et al. (2025) design, with three or more well-chosen distractors, respondents virtually never report having noticed the repeat, so Assumption 2 holds empirically. Under all three assumptions, \(\Delta \in [0, 1]\) in principle, but the practical maximum is \(0.5\); the value implied by independent Bernoulli draws.

29.6.3 Why \(\bar D\) is preferred to test–retest correlation

For binary items, \(\bar D\) contains strictly more information for analytic purposes than the test–retest correlation, for three reasons.

First, \(\bar D\) is on the same scale as the outcome (probability of disagreement), whereas correlation is unitless and harder to translate into substantive terms.

Second, \(\bar D\) has a direct decision-theoretic interpretation: it tells you the probability that an arbitrarily selected respondent’s recorded answer would differ if you collected the data again moments later. No correlation coefficient gives you that quantity directly.

Third, \(\bar D\) does not depend on the marginal distribution of the outcome, while correlation does. The classical relationship is

\[\begin{equation} r_{tt} \;=\; 1 - \frac{\bar D}{2 p (1-p)}, \tag{29.4} \end{equation}\]

where \(p = \Pr(C = 1)\). Equation (29.4) makes the marginal dependence explicit: holding \(\bar D\) fixed, \(r_{tt}\) shrinks toward zero as \(p\) approaches \(\tfrac{1}{2}\). This is the binary-item version of the classical fact that polychoric and Pearson correlations on dichotomised data depend on marginals; Achen (1975) gives the canonical political-behaviour treatment, and the broader psychometric literature (Alwin 2007) confirms the same pattern for ordinal items.

Table 29.9 makes the dependence concrete: for a fixed \(\bar D = 0.20\), the implied \(r_{tt}\) varies from 0.60 at \(p = 0.5\) down to 0.38 at \(p = 0.2\). A reader who reads only \(r_{tt}\) would draw very different conclusions about the same underlying response process depending on the marginal.

| D-bar | p = Pr(C=1) | r_tt |

|---|---|---|

| 0.1 | 0.5 | 0.800 |

| 0.1 | 0.3 | 0.762 |

| 0.1 | 0.2 | 0.688 |

| 0.2 | 0.5 | 0.600 |

| 0.2 | 0.3 | 0.524 |

| 0.2 | 0.2 | 0.375 |

| 0.3 | 0.5 | 0.400 |

| 0.3 | 0.3 | 0.286 |

| 0.3 | 0.2 | 0.062 |

We therefore recommend reporting \(\bar D\) as the primary reliability statistic for binary survey items, with the test–retest correlation reported alongside only if comparison to historical literature requires it.

29.6.4 Sampling distribution of \(\bar D\)

Because \(D_i \in \{0,1\}\) and is sampled independently across respondents under simple random sampling, \(\bar D\) is the sample mean of independent Bernoulli\((\Delta)\) random variables with population variance \(\Delta(1-\Delta)\). The standard error is

\[\begin{equation} \mathrm{SE}(\bar D) \;=\; \sqrt{\frac{\Delta(1-\Delta)}{n}} \;\approx\; \sqrt{\frac{\bar D(1-\bar D)}{n}}. \tag{29.5} \end{equation}\]

A two-sided \(1 - \alpha\) Wald interval from equation (29.5) is \(\bar D \pm z_{1-\alpha/2}\,\mathrm{SE}(\bar D)\). For small samples or for \(\bar D\) near 0 or 0.5, the Clopper–Pearson exact interval or a Wilson score interval should be preferred to Wald. We illustrate both in Section 29.15.

For non-binary items, the natural generalisation of \(\bar D\) is the within-respondent mean absolute discrepancy or, for ordinal items, the within-respondent Spearman rank correlation across replications. The mathematical apparatus changes; the conceptual point, use a within-session replicated DV to identify intrinsic stochasticity, does not.

29.7 Classical reliability theory and where it stops

Before we develop the three-way variance decomposition we need to be precise about what classical psychometrics already provides. The argument of this chapter is not that classical reliability theory is wrong; it is that it is silent on a specific component of the noise. Knowing exactly what classical theory does identify is a precondition for seeing what it does not.

29.7.1 The classical decomposition

The foundational reference is Lord and Novick (1968). An observed score \(X\) is decomposed into a true score \(T\) and an error term \(E\),

\[\begin{equation} X \;=\; T + E,\qquad \mathrm{Var}(X) \;=\; \mathrm{Var}(T) + \mathrm{Var}(E), \tag{29.6} \end{equation}\]

with \(\mathrm{Cov}(T, E) = 0\) by construction. The reliability of the measurement is

\[\begin{equation} \rho \;=\; \frac{\mathrm{Var}(T)}{\mathrm{Var}(T) + \mathrm{Var}(E)} \;=\; 1 - \frac{\mathrm{Var}(E)}{\mathrm{Var}(X)}, \tag{29.7} \end{equation}\]

a number in \([0, 1]\). The standard estimators of \(\rho\) in equation (29.7) depend on the nature of the data.

29.7.2 Cronbach’s \(\alpha\) for multi-item scales

When the measurement is a \(k\)-item scale, the standard internal-consistency estimator is Cronbach (1951)’s \(\alpha\),

\[\begin{equation} \alpha \;=\; \frac{k}{k - 1} \left( 1 - \frac{\sum_{j=1}^{k} \mathrm{Var}(X_j)}{\mathrm{Var}\!\left(\sum_{j=1}^{k} X_j\right)} \right), \tag{29.8} \end{equation}\]

Equation (29.8) is a lower bound on \(\rho\) under the assumption of \(\tau\)-equivalent items. Cronbach’s \(\alpha\) is silent on within-respondent within-item noise; it summarises across-item consistency. A scale with \(\alpha = 0.95\) can still produce \(\bar D = 0.25\) on each individual item.

29.7.3 Coefficient \(\omega\) as a superior alternative to \(\alpha\)

Cronbach’s \(\alpha\) is the field’s default reliability statistic, but psychometricians have argued for decades that it is a poor lower bound and a worse point estimate of true reliability whenever the \(\tau\)-equivalence assumption fails. The modern alternative is McDonald (1999)’s coefficient \(\omega\), derived from a factor-analytic representation of the scale. For a single-factor scale with loadings \(\lambda_j\) and item residual variances \(\psi_j^2\), the total-score reliability is

\[\begin{equation} \omega_t \;=\; \frac{(\sum_{j} \lambda_j)^2}{(\sum_{j} \lambda_j)^2 + \sum_{j} \psi_j^2}. \tag{29.9} \end{equation}\]

For congeneric scales, \(\omega_t \ge \alpha\) in equation (29.9), and equality holds only under \(\tau\)-equivalence (equal loadings). Revelle and Zinbarg (2009) argue that \(\alpha\) should be retired in favour of \(\omega_t\) for the total-score reliability and \(\omega_h\) for the proportion of variance attributable to a general factor; the psych package in R reports all three. For the reliability-reporting practitioner, the recommendation is to report \(\omega_t\) alongside \(\alpha\) until the field’s reporting conventions catch up.

29.7.4 Generalizability theory

Classical test theory partitions variance into a single true-score component and a single error component (equation (29.6)). Generalizability theory (Cronbach et al. 1972) generalises this partition to multiple identified facets of variance: items, raters, occasions, and any other source whose variance the analyst wants to identify separately. The framework yields generalizability coefficients \(E\rho^2\) tailored to specific decision contexts (absolute vs. relative interpretation) and allows the analyst to project how reliability would change under alternative measurement designs (more items, more raters, more occasions).

G-theory is the natural home of the three-way decomposition in equation (29.11): intrinsic stochasticity is a respondent-by-occasion variance component that G-theory makes first-class. The gtheory R package implements the standard variance-components estimation. We mention G-theory here as the right framework for the analyst who wants to push the variance decomposition further than this chapter does.

29.7.5 Test–retest correlation and the Heise–Wiley simplex

For longitudinal designs, the natural reliability estimator is the test–retest correlation \(r_{tt}\) defined in equation (29.4). The classical objection (Heise 1969; Wiley and Wiley 1970) is that for any non-zero interval between administrations, \(r_{tt}\) confounds unreliability (within-respondent measurement noise) with true change (within-respondent attitude shift).

Heise (1969) shows that with three administrations of the same item it is possible to separate reliability from stability using the moment conditions of an autoregressive measurement model. Let \(X_t\) denote the observed score at time \(t\), \(T_t\) the latent true score, and assume

\[\begin{align} X_t &= T_t + E_t, & E_t &\sim \mathcal{N}(0, \sigma_E^2),\ \mathrm{independent\ across}\ t, \\ T_t &= \beta_t T_{t-1} + U_t, & U_t &\sim \mathcal{N}(0, \sigma_U^2). \end{align}\]

The identification of the Heise estimators below requires the stationarity assumption that \(\mathrm{Var}(T_t)\) is time-invariant, so that reliability \(\rho = \mathrm{Var}(T_t)/\mathrm{Var}(X_t)\) is constant across waves; Wiley and Wiley (1970) relaxes this assumption at the cost of an additional wave and develops a maximum-likelihood version of the simplex that admits time-varying error variances. Under the stationarity assumption, with three waves, the three pairwise correlations \(r_{12}\), \(r_{23}\), \(r_{13}\) over-identify \((\rho, \beta_1, \beta_2)\), yielding the Heise estimators

\[\begin{equation} \hat\rho_2 \;=\; \frac{r_{12} \cdot r_{23}}{r_{13}},\qquad \hat\beta_1 \;=\; \frac{r_{13}}{r_{23}},\qquad \hat\beta_2 \;=\; \frac{r_{13}}{r_{12}}. \tag{29.10} \end{equation}\]

The Heise–Wiley simplex remains the classical workhorse for longitudinal reliability estimation in sociology and political science.

Why the simplex is silent on intrinsic stochasticity. The simplex identifies \(\rho\) and \(\beta_t\) from across-wave covariances that assume independent measurement error across waves. If part of the residual noise is, in fact, intrinsic stochasticity drawn afresh from a respondent-level distribution at each measurement, the simplex absorbs it into \(\sigma_E^2\) and labels it “measurement error”. The decomposition is internally consistent, but the substantive interpretation; “this is noise we could in principle eliminate with a better instrument”; is wrong.

29.7.6 Multi-trait multi-method reliability

Saris and Gallhofer (2014) gives the modern Wiley-style synthesis. The MTMM (multi-trait multi-method) design administers each of \(T\) traits through each of \(M\) methods, yielding \(TM\) measurements per respondent and identification of trait variance, method variance, and unique variance from a structural equation model. MTMM is the gold-standard reliability assessment in survey methodology, but it shares the simplex’s limitation: any noise drawn from a respondent-level stochastic process at each measurement is absorbed into the unique-variance term and is not separately identified.

The within-survey replicated DV protocol (Section 29.12) is, in this language, a single-trait single-method design with within-session replication; what it gives up in trait/method coverage it gains in the ability to isolate intrinsic stochasticity from instrument noise.

29.8 A three-way variance decomposition

The classical decomposition in equation (29.6) lumps everything that is not signal into a single residual. We argue it should be replaced with

\[\begin{equation} \mathrm{Var}(X) \;=\; \underbrace{\mathrm{Var}(T)}_{\text{signal}} \;+\; \underbrace{\mathrm{Var}(M)}_{\text{measurement error}} \;+\; \underbrace{\mathrm{Var}(S)}_{\text{intrinsic stochasticity}}, \tag{29.11} \end{equation}\]

In equation (29.11), \(T\), \(M\), and \(S\) are pairwise uncorrelated. The third term captures noise that is part of the respondent’s response-generation process rather than a defect of the instrument. The new reliability ratio is

\[\begin{equation} \rho^{\ast} \;=\; \frac{\mathrm{Var}(T)}{\mathrm{Var}(T) + \mathrm{Var}(M) + \mathrm{Var}(S)}, \tag{29.12} \end{equation}\]

The \(\rho^{\ast}\) defined in equation (29.12) satisfies \(\rho^{\ast} \le \rho\) in general. The classical \(\rho\) confuses \(\mathrm{Var}(M) + \mathrm{Var}(S)\) for a single residual; \(\rho^{\ast}\) separates them.

This is not a semantic distinction. It has direct empirical consequences (Table 29.10).

| Question | Two-way (Lord-Novick) | Three-way (this chapter) |

|---|---|---|

| Will instrument improvement reduce the residual? | Always yes (by definition) | Only \(\mathrm{Var}(M)\); \(\mathrm{Var}(S)\) irreducible |

| Is the residual identified by within-session replication? | Yes | \(\mathrm{Var}(M) + \mathrm{Var}(S)\) identified jointly |

| Is the residual identified by classical test–retest? | Yes (with caveats; see Heise simplex) | \(\mathrm{Var}(S)\) absorbed into the error term |

| Does the residual attenuate regression coefficients? | Yes, by attenuation factor | Yes for \(\mathrm{Var}(M)\); the \(\mathrm{Var}(S)\) part needs the correction in Section 29.14.3 |

| Does the residual cancel out in differences (DiD, RDD)? | Yes, on average | Yes for both, on average |

The three-way decomposition is not unique to survey research. Table 29.12 lists analogous decompositions in adjacent disciplines.

| Field | Instrument-side variance | Subject-side variance |

|---|---|---|

| Survey research (this chapter) | Measurement error (M) | Intrinsic stochasticity (S) |

| Gene-expression noise (Elowitz et al. 2002) | Extrinsic noise | Intrinsic gene-expression noise |

| fMRI / neuroimaging | Thermal / scanner noise | Physiological / spontaneous activity |

| Soft-matter / colloid physics | Diffraction / optical limits | Brownian motion |

| Classical test theory (Lord and Novick 1968) | Error of measurement | True-score variation |

The analogy with gene-expression noise is particularly tight. Elowitz et al. (2002) separated intrinsic and extrinsic contributions to noise in protein expression by simultaneously measuring two identical fluorescent reporters in the same cell; the within-cell discrepancy is intrinsic, the across-cell discrepancy after subtracting intrinsic noise is extrinsic. The within-survey replicated DV plays an exactly analogous role: it isolates the within-respondent noise component that no instrument-side fix can remove.

The implication for applied analysts is direct. When you observe a \(\bar D\) of, say, 0.20 in a binary outcome and you have already done the careful work of debiasing your instrument, do not conclude that you have failed. Conclude that you are approaching the irreducible floor for your population and item, and adjust your inference and your reporting accordingly.

29.9 Decision-theoretic foundations

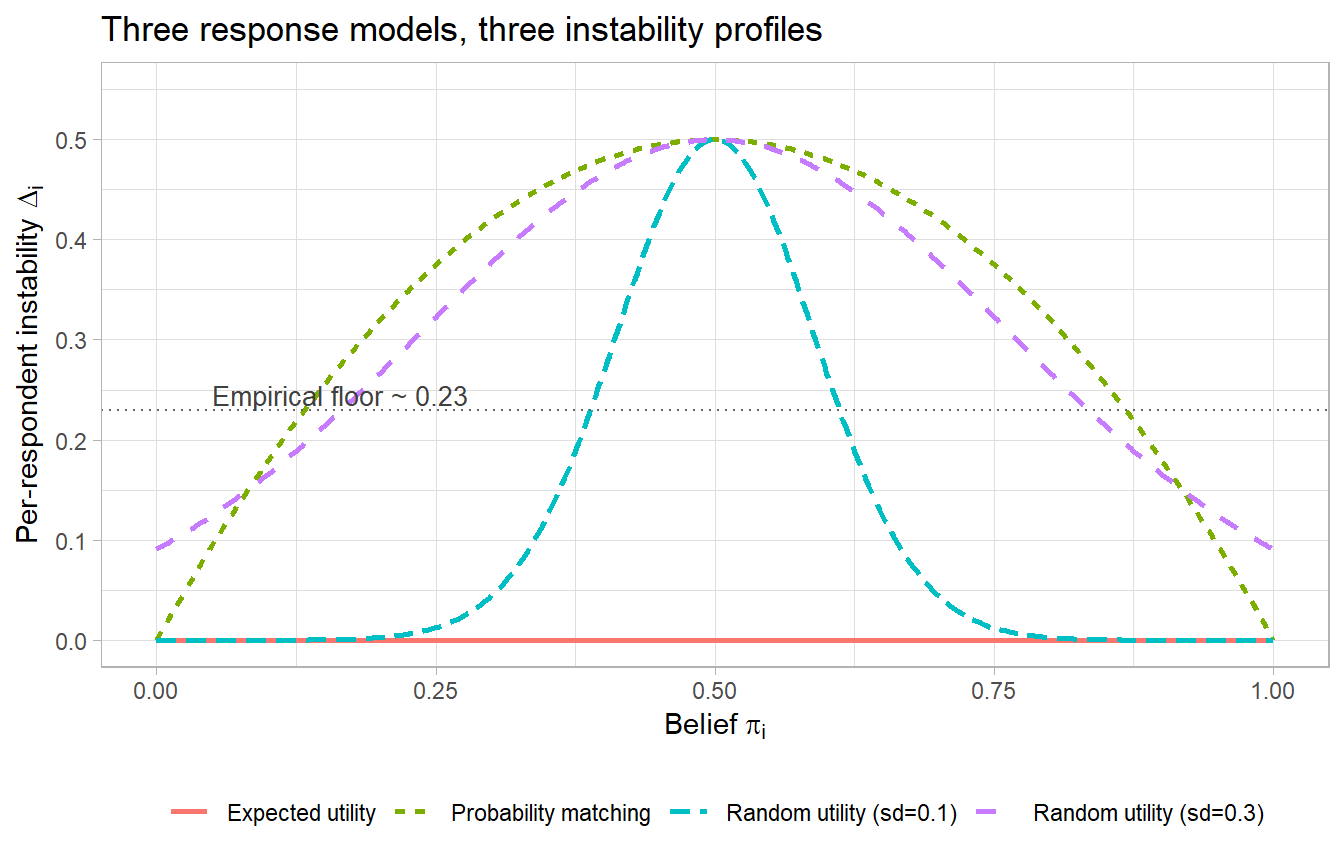

The presence of intrinsic stochasticity raises a question that classical reliability theory does not answer: through what mechanism does noise enter the response? A complete answer requires a model of how respondents transform their (potentially uncertain) preferences into observed choices. We review three candidate models in order of increasing realism.

29.9.1 Expected utility (deterministic)

Let \(\theta_i \in \{0, 1\}\) denote respondent \(i\)’s true preference (we use \(\theta\) rather than \(\rho\) to avoid collision with the classical reliability ratio \(\rho\) of Section 29.7) and \(\pi_i \in [0,1]\) their belief that \(\theta_i = 1\). Under expected utility (with no idiosyncratic shocks), the respondent always picks the option more likely to be correct,

\[\begin{equation} C_{it} \;=\; \mathbb{1}\!\left( \pi_i > 0.5 \right). \tag{29.13} \end{equation}\]

Under (29.13), \(\pi_{i1} = \pi_{i2}\) implies \(C_{i1} = C_{i2}\) for every respondent, hence \(D_i = 0\) for every respondent who knows their own preference. This model predicts zero observed instability, which is empirically false at any reasonable sample size.

29.9.2 Random utility (stochastic input, deterministic decision rule)

The economics-flavoured fix, foundational in discrete-choice modelling, is to add a mean-zero shock just before the decision,

\[\begin{equation} C_{it} \;=\; \mathbb{1}\!\left( \pi_i + \eta_{it} > 0.5 \right),\qquad \eta_{it} \perp \!\!\! \perp \eta_{is}\ \text{for}\ t \neq s, \tag{29.14} \end{equation}\]

where \(\eta_{it}\) is drawn afresh on each administration. This is the foundation of all logit and probit discrete-choice models, including the Hainmueller et al. (2014) AMCE estimator. Under (29.14), instability is positive but vanishes as \(|\pi_i - 0.5|\) grows large or as \(\mathrm{Var}(\eta_{it})\) shrinks to zero. The per-respondent instability is

\[\begin{equation} \Delta_i^{\mathrm{RUM}} \;=\; 2\, p_i (1 - p_i),\qquad p_i \;=\; \Pr(\pi_i + \eta_{it} > 0.5), \tag{29.15} \end{equation}\]

Equation (29.15) is a strictly decreasing function of \(|\pi_i - 0.5|\) for any unimodal symmetric shock. RUM is consistent with Kahneman and Tversky (1979) prospect-theoretic deviations from expected utility insofar as the deviations enter as mean-zero shocks; it is not consistent with intrinsically stochastic choice.

29.9.3 Probability matching (irreducibly stochastic)

The psychology-flavoured alternative treats the choice itself as stochastic, even when beliefs are perfectly known:

\[\begin{equation} C_{it} \;\sim\; \mathrm{Bernoulli}(\pi_i),\qquad C_{i1} \perp \!\!\! \perp C_{i2}\mid \pi_i. \tag{29.16} \end{equation}\]

Under (29.16), even a respondent who is perfectly informed about \(\pi_i\) does not necessarily choose the higher-probability option. The expected per-respondent instability is

\[\begin{equation} \Delta_i^{\mathrm{PM}} \;=\; 2\, \pi_i (1 - \pi_i), \tag{29.17} \end{equation}\]

Equation (29.17) is strictly positive whenever \(\pi_i \in (0, 1)\) and reaches its maximum of \(0.5\) at \(\pi_i = 0.5\). Probability matching has been documented in humans, primates, fish, pigeons, and bees, and remains one of the most replicated findings in experimental decision science despite half a century of attempts to design it away (Vulkan 2000; Lo et al. 2021). The phenomenon is not merely a curiosity: in incentivised financial-decision experiments, even subjects with statistical training systematically randomise rather than maximise (Lo et al. 2021), and reinforcement-learning models that predict probability-matching emerge naturally fit experimental game-play data (Erev and Roth 1998).

29.9.4 Why this matters for applied analysts

Suppose you fit a binary logit to a survey outcome. The standard interpretation treats the linear predictor as the systematic part and the logit shock as measurement-error-like noise. If respondents are in fact probability-matching, the logit shock is not error in the classical sense; it is a property of the respondent’s decision process. Two consequences follow.

First, the conditional choice probabilities \(\widehat{\Pr}(C = 1 \mid X)\) recovered from a logit can be biased toward \(0.5\) when respondents probability-match, because the model assumes deterministic-conditional-on-shock choice when in fact the choice is irreducibly Bernoulli\((\pi)\). Clayton et al. (2025) derive the corresponding correction for forced-choice conjoint experiments under the Hainmueller et al. (2014) AMCE framework.

Second, treating intrinsic stochasticity as classical errors-in-variables in the response will not help, because the classical errors-in-variables apparatus assumes the noise is in the regressor. Under probability matching, the noise is in the response itself, which produces a different attenuation pattern (Section 29.14.3).

A simple simulation makes the qualitative differences vivid. Figure 29.3 plots \(\Delta_i\) as a function of \(\pi_i\) under each of the three models.

library(ggplot2)

library(dplyr)

library(tidyr)

pi_grid <- tibble(pi = seq(0, 1, length.out = 401))

eu_instab <- function(pi) rep(0, length(pi))

pm_instab <- function(pi) 2 * pi * (1 - pi)

rum_instab <- function(pi, sd) {

p <- 1 - pnorm(0.5 - pi, sd = sd)

2 * p * (1 - p)

}

sim_df <- pi_grid |>

mutate(

`Expected utility` = eu_instab(pi),

`Probability matching` = pm_instab(pi),

`Random utility (sd=0.1)` = rum_instab(pi, sd = 0.1),

`Random utility (sd=0.3)` = rum_instab(pi, sd = 0.3)

) |>

pivot_longer(-pi, names_to = "model", values_to = "instability")

ggplot(sim_df, aes(pi, instability, colour = model, linetype = model)) +

geom_line(linewidth = 1) +

geom_hline(yintercept = 0.23, linetype = "dotted", colour = "grey40") +

annotate("text", x = 0.05, y = 0.245,

label = "Empirical floor ~ 0.23",

hjust = 0, size = 3.5, colour = "grey25") +

scale_y_continuous(limits = c(0, 0.55), breaks = seq(0, 0.5, 0.1)) +

labs(x = expression(paste("Belief ", pi[i])),

y = expression(paste("Per-respondent instability ", Delta[i])),

colour = NULL, linetype = NULL,

title = "Three response models, three instability profiles") +

theme(legend.position = "bottom")

Figure 29.3: Per-respondent instability \(\Delta_i\) as a function of the underlying belief \(\pi_i\) under three response models. Probability matching predicts a smooth quadratic peaking at \(\pi_i = 0.5\) with \(\Delta_i = 0.5\). Random utility with small shocks predicts a sharp peak near \(\pi_i = 0.5\). Expected utility predicts identically zero. Empirically observed instability profiles are most consistent with the probability-matching curve.

Figure 29.3 makes three things clear. First, expected utility predicts zero instability for every respondent, regardless of \(\pi_i\). Second, probability matching peaks at \(\pi_i = 0.5\) with \(\Delta_i = 0.5\) and decreases as beliefs become more certain, but never reaches zero except at the endpoints. Third, random utility with small noise is concentrated near \(\pi_i = 0.5\); with larger noise it spreads out and approaches the probability-matching curve in shape, although the underlying process is different.

29.10 Beyond the decision model: what modulates stochasticity

Once we accept that decision making is stochastic, we can ask what modulates the magnitude of that stochasticity. The empirical literature in survey methodology and cognitive psychology organises the answer at four nested levels of proximity to the response.

29.10.1 The cognitive process level

Three modulators have direct survey-design implications.

Cognitive complexity. Items requiring more cognitive resources (longer questions, more response options, unfamiliar phrasing) produce more instability. Time-on-task averaged across respondents is a usable proxy for complexity, although confounded with attentiveness within respondents. The classical analysis of how respondents shortcut effortful retrieval and integration; satisficing in Krosnick (1991) and Krosnick (1999); describes the cognitive mechanism through which complexity inflates intrinsic stochasticity: when retrieval is costly, a respondent samples partial evidence and integrates it noisily.

Time on task within respondents. Below an item-specific threshold, instability rises sharply toward \(0.5\). Above the threshold, instability stabilises near the population baseline. Where the platform allows, hidden-page time can be subtracted using the Page Visibility API to recover attended time on task; when this is unavailable, raw on-page time is an upper bound on attended time. We give a calibration procedure in Section 29.15.

Divergent processing across administrations. Even with adequate time, respondents who attend to the item differently the second time produce more instability. This has been measured experimentally with eye-tracking; for most applications, it cannot be measured directly but motivates careful attention to priming differences between the two administrations.

29.10.2 The psychological state level

Four states have been studied as candidate filters for poor data quality. They differ in whether they are (a) consciously controllable, (b) influenced by other survey items, and (c) themselves stable within a single session. Table 29.13 summarises.

| State | Influenced by other items? | Under conscious control? | Stable within session? |

|---|---|---|---|

| Preoccupation | No | No | Yes |

| Mind-wandering | Yes | No | No |

| Persona / mood self-report | No | Yes | No |

| Attention checks (IMC) | Yes | Yes | No |

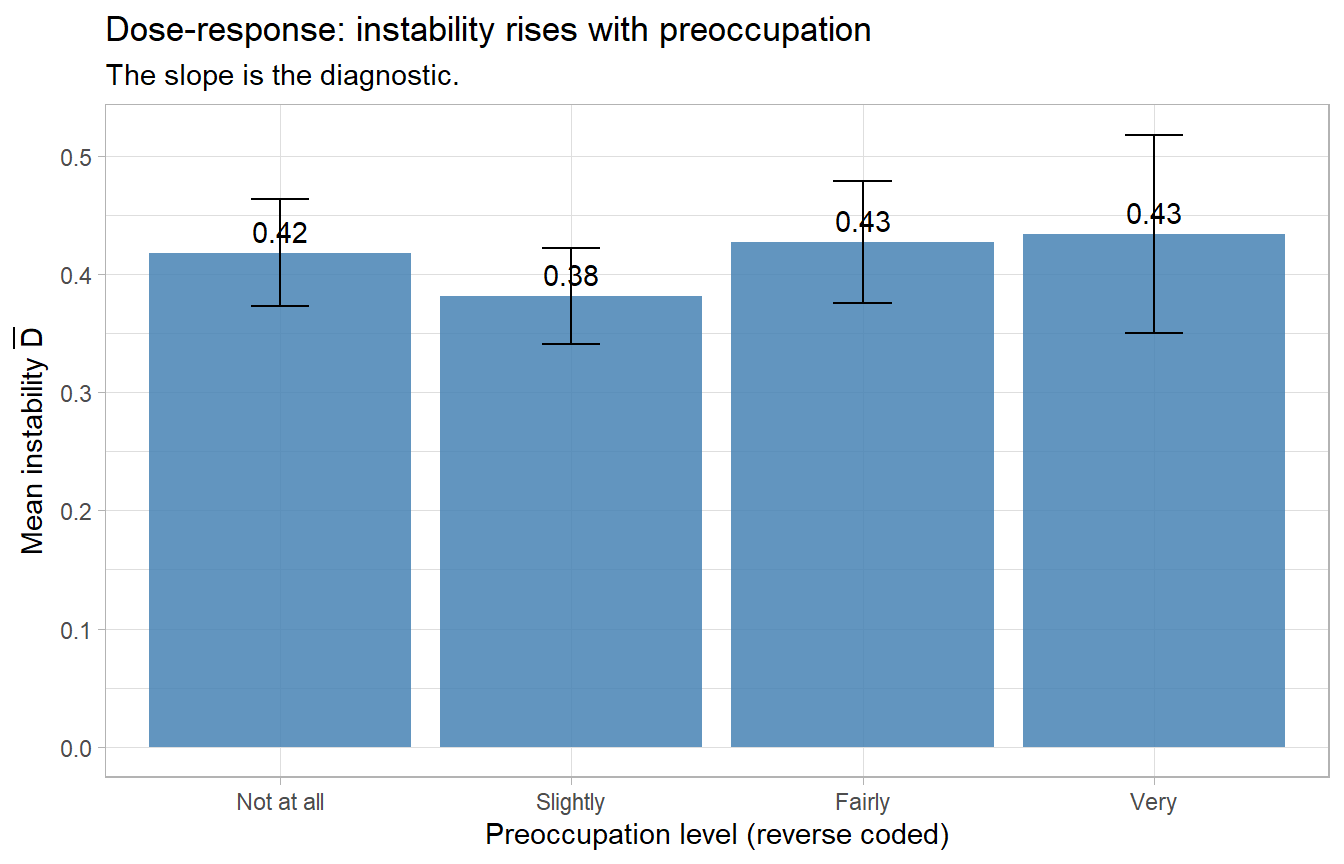

Only preoccupation satisfies all three properties shown in Table 29.13. The others are useful as research variables but problematic as primary filters. The five-criterion evaluation appears in Section 29.11.

29.10.3 The individual-characteristic level

Demographics, socioeconomic position, and prior knowledge predict instability. Older respondents, despite slower cognition, often exhibit lower instability than younger respondents, apparently because they are less preoccupied and mind-wander less. This is not a license to filter respondents on age (doing so would change the estimand), but it is useful diagnostic information and motivates always reporting \(\bar D\) stratified by key demographics.

The literature on response styles (Krosnick 1999; Schwarz 1999) identifies several individual-level patterns relevant here: acquiescence (the tendency to agree regardless of content), extreme responding (preferring scale endpoints), and central tendency (preferring scale midpoints). All three inflate \(\bar D\) when an item flips its semantic polarity between administrations, which is one reason within-session replication should keep wording identical. Social-desirability response bias (Crowne and Marlowe 1960; Tourangeau and Smith 1996) is a separate but related concern: respondents systematically misreport on sensitive items in a direction that conforms to perceived norms; this biases the estimated \(\Pr(C = 1)\) but does not necessarily inflate \(\bar D\) unless the perceived norm shifts between administrations.

29.10.4 The item characteristic level

Items differ in their susceptibility to all of the above. The single best predictor of an item’s \(\bar D\) is its position on a complexity scale, calibrated by either expert rating or pre-test mean TOT. Krosnick (1999)’s review of question-design effects, together with Schuman and Presser (1981)’s extensive catalog of wording experiments, gives the analyst a working menu of item features that inflate \(\bar D\):

- Double-barrelled questions (combining two propositions in one item).

- Negatively worded items, especially those embedded among positively worded ones.

- Items with more than seven response options on a non-anchored scale.

- Items requiring specific numerical estimates (“how many times in the past month did you…”).

- Items referring to events more than three months in the past.

These are the items where pre-testing is most valuable and where within-session replication is most informative. Items at the simple end; bipolar attitude items with five or fewer well-anchored response options, asked once; contribute relatively little to total \(\bar D\) even in long instruments.

29.11 Filter design: five criteria

Filtering respondents to improve data quality is necessary but risky. A good filter must satisfy all five of the following criteria.

- Exogeneity to other survey items. The filter is not influenced by the content of the rest of the survey.

- Exogeneity to conscious choice. The respondent cannot easily produce the “correct” answer to escape the filter.

- Predictive validity. The filter actually predicts instability or other markers of poor data quality.

- No treatment effect on other items. Including the filter item does not change responses to subsequent items.

- Within-survey stability. The filter item itself is stable across the duration of the survey.

The empirical evidence evaluates four candidate filters against these criteria; Table 29.14 summarises.

| Filter |

|

|

|

|

|

Verdict |

|---|---|---|---|---|---|---|

| Preoccupation | Yes | Yes | Yes | Yes | Yes | Use as primary |

| Mind-wandering probe | No | Yes | Yes | Yes | No | Research only |

| Persona / mood self-report | Yes | No | Yes | Yes | No | Research only |

| Attention checks (IMC) | No | No | Mixed | No | No | Avoid as primary |

29.11.1 The case against attention checks as a primary filter

The instructional manipulation check (IMC) of Oppenheimer et al. (2009) is still the most widely deployed quality filter in online survey research. The empirical critique of the IMC as a primary filter is threefold.

First, including an IMC changes how respondents read subsequent items, treating each as a potential trick rather than a sincere question, a violation of Gricean cooperative norms documented in Oppenheimer et al. (2009). This is a violation of criterion (4) in Table 29.14.

Second, pass rates on commonly used IMCs vary from approximately one third to nearly the whole sample across populations, formulations, and platforms (Berinsky et al. 2014, 2012; Hauser and Schwarz 2016). The filter is not measuring a stable construct, in violation of criterion (5).

Third, dropping respondents who fail an IMC introduces selection on observables that correlate with the outcome. Aronow et al. (2019) derive the formal bias and show it is non-ignorable in the standard randomised-experiment-with-survey-DV setting; Berinsky et al. (2014) document that screener pass rates correlate with politically and demographically relevant respondent characteristics, so dropping failers re-defines the population.

The cumulative case is not that IMCs are useless (they remain valuable as research diagnostics and, in some venues, as reviewer-expected reassurance) but that they are a poor primary filter.

29.11.2 Multivariate detection of careless responding

The careless-responding literature (Meade and Craig 2012; Curran 2016; Ward and Meade 2023) develops a battery of detection indices that go beyond the single IMC. Five families recur in the literature.

- Long-string indices. The maximum number of consecutive identical responses; long strings suggest non-effortful straightlining.

- Inter-item standard deviation. The within-respondent SD across reverse-coded item pairs; near-zero SD on a heterogeneous scale suggests acquiescence.

- Person-total correlation. The correlation between the respondent’s vector of answers and the sample-mean answer vector; very low or negative values are anomalous.

- Mahalanobis distance. Multivariate outlier detection on the response vector.

- Response time outliers. TOT below an item-specific floor (Section 29.12).

Meade and Craig (2012) recommend computing several of these indices in parallel and using the joint distribution to flag respondents, rather than dropping on any single index. Ward and Meade (2023)’s Annual Review of Psychology synthesis is the current best entry point: it consolidates prevention (instrument design, instructed-response items), identification (the indices above plus consistency-based families), and reporting recommendations. Prevalence baselines come from Necka et al. (2016), who report problematic-respondent rates side by side for MTurk, campus, and community samples and find that the composition of careless responses, rather than the rate per se, differs across recruitment sources. The recommendation in this chapter is consistent with both: report the indices, flag rather than drop, and disclose the joint distribution alongside the substantive analysis.

29.11.3 The recommended primary filter: preoccupation

A validated four-level preoccupation item is administered immediately after consent and before any focal items. A workable wording is

Everyone comes to a new task (like this survey) with things on their minds. How preoccupied were you, just before you started this survey, with thoughts or worries about your partner, job, health, children, friends, money, or other concerns?

(1) Very preoccupied; (2) Fairly preoccupied; (3) Slightly preoccupied; (4) Not at all preoccupied.

Treat the response as a four-level ordinal variable. Do not drop respondents on the basis of preoccupation alone, because doing so changes the estimand: the resulting sample no longer represents the population on a variable correlated with the outcome. Instead, flag preoccupied respondents and report estimates with and without the flagged subset side by side. This preserves the population-level estimand while signalling to readers how much the conclusion depends on the most-preoccupied respondents.

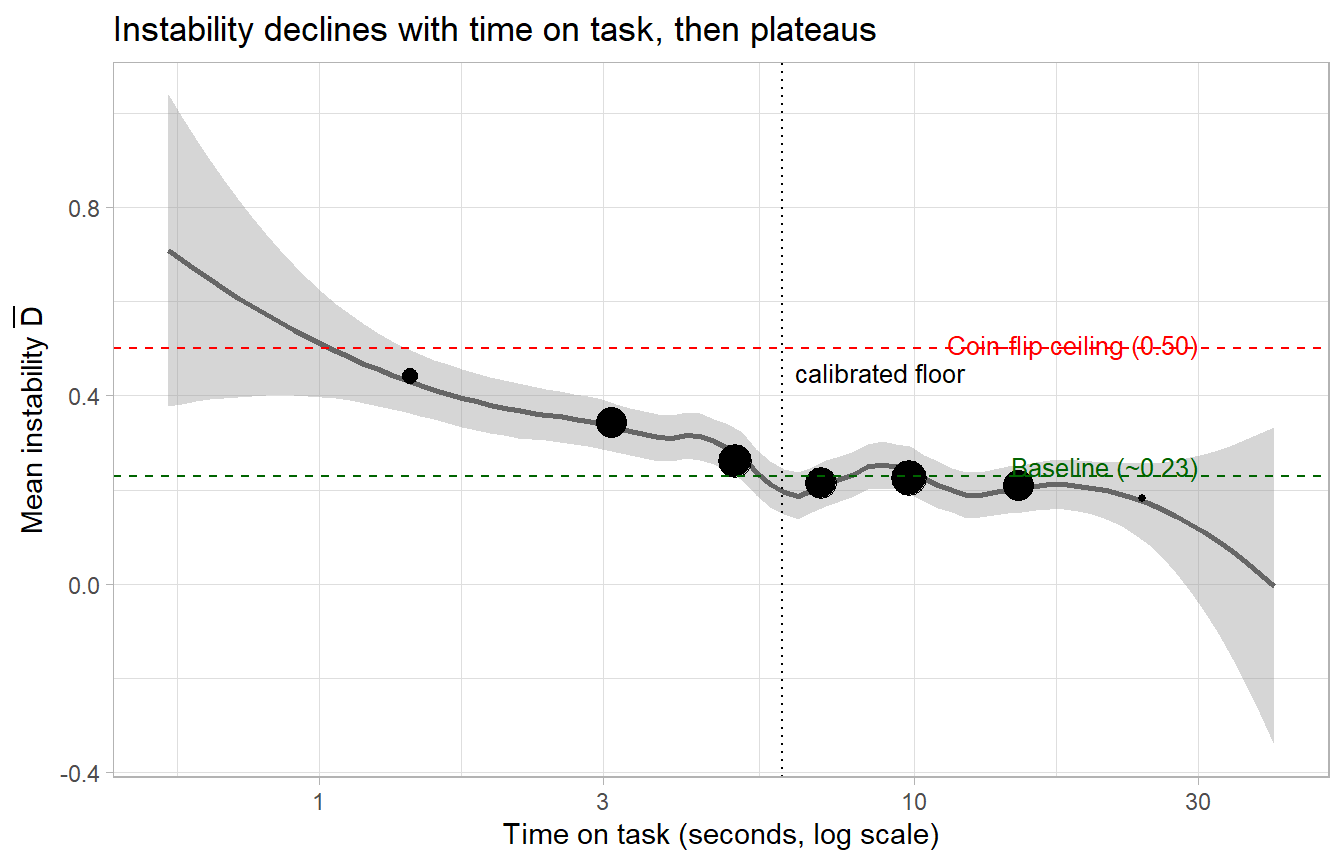

29.12 Time on task as an exogenous quality measure

The second recommended quality signal is time on task (TOT), measured on burn-in items rather than focal items. The distinction matters: TOT on the focal item is endogenous (a respondent may be slow because the item is hard, because they are preoccupied, or because they are attentive; you cannot separate these post hoc), whereas TOT on burn-in items provides an exogenous reading.

A practical workflow is:

- Insert two or three burn-in items between the preoccupation item and the first focal item. Match their format to the focal items (conjoint, Likert, multiple choice).

- Record TOT in seconds for each burn-in item.

- Compute the mean TOT across burn-in items per respondent.

- Apply a cognitive-complexity-appropriate floor. The floor is item-specific and must be calibrated empirically; see Step 2 in Section 29.15 for a calibration procedure.

Figure 29.4 gives a simulated illustration of the TOT–instability relationship.

library(dplyr)

library(ggplot2)

set.seed(123)

n <- 2000

tot_seconds <- rgamma(n, shape = 2, scale = 4) + 0.5

true_instability <- pmin(0.5, 0.5 - 0.28 * (1 - exp(-0.4 * (tot_seconds - 1))))

true_instability <- pmax(true_instability, 0.22)

D_obs <- rbinom(n, 1, true_instability)

tot_df <- tibble(tot = tot_seconds, D = D_obs) |>

mutate(tot_bin = cut(tot,

breaks = c(0, 2, 4, 6, 8, 12, 20, 60),

include.lowest = TRUE))

bin_summary <- tot_df |>

group_by(tot_bin) |>

summarise(D_mean = mean(D),

n_in_bin = dplyr::n(),

tot_mid = mean(tot),

.groups = "drop")

ggplot(bin_summary, aes(tot_mid, D_mean)) +

geom_smooth(data = tot_df, aes(tot, D), method = "loess", se = TRUE,

span = 0.4, inherit.aes = FALSE, colour = "grey40") +

geom_point(aes(size = n_in_bin)) +

geom_hline(yintercept = 0.50, linetype = "dashed", colour = "red") +

geom_hline(yintercept = 0.23, linetype = "dashed", colour = "darkgreen") +

geom_vline(xintercept = 6, linetype = "dotted") +

annotate("text", x = 30, y = 0.51, label = "Coin-flip ceiling (0.50)",

colour = "red", size = 3.4, hjust = 1) +

annotate("text", x = 30, y = 0.25, label = "Baseline (~0.23)",

colour = "darkgreen", size = 3.4, hjust = 1) +

annotate("text", x = 6.3, y = 0.45, label = "calibrated floor",

size = 3.4, hjust = 0) +

scale_x_log10() +

scale_size_continuous(guide = "none") +

labs(x = "Time on task (seconds, log scale)",

y = expression(paste("Mean instability ", bar(D))),

title = "Instability declines with time on task, then plateaus")

Figure 29.4: Simulated time-on-task vs. instability relationship. Below an item-specific threshold (around 6 seconds for the conjoint-style items used here), instability rises sharply toward the coin-flip ceiling. Above the threshold, instability stabilises near the baseline rate. The threshold value depends on item complexity and must be calibrated for each instrument.

Two implementation notes follow from Figure 29.4. First, measured TOT is an upper bound on actual attention time, since a respondent may have the item on screen while mind-wandering or tab-switching. Where the platform allows, subtract hidden-page time. Second, dropping respondents who fall below the floor on burn-in items is a less risky filter than preoccupation-based dropping because the floor cleanly identifies inattentive respondents who could not have read the item, and the dropped group is far less correlated with substantive outcomes than the dropped-on-preoccupation group would be.

The mode-effects literature (Holbrook et al. 2003) is relevant here: telephone respondents satisfice more than face-to-face respondents and produce systematically different TOT distributions on the same item. When pooling across modes, calibrate the TOT floor mode-by-mode rather than once for the pooled sample.

29.13 Practical implications for survey design

The argument has direct implications for how surveys should be designed. We list them in approximate order of importance.

- Reduce cognitive complexity. Write items in respondents’ vocabulary, not researchers’ vocabulary (Krosnick 1999; Saris and Gallhofer 2014; Dillman et al. 2014). Prefer four response options to seven. Avoid double-barrelled questions, branching scales, and clauses that require sustained working memory. Pretest with timing, and flag items where mean TOT exceeds 30 seconds. Dillman et al. (2014)’s Tailored Design Method is the standard practitioner reference on questionnaire layout, contact protocols, and mode-specific design choices; for any first-time-survey project we recommend it as a complement to the cognitive-side guidance in this chapter.

- Always measure \(\bar D\) on the key dependent variable. Insert the same item a second time, separated by at least three distractor items, and compute \(\bar D\) as part of the standard analysis. This is the single most important addition to survey reporting standards we can recommend.

- Replace IMCs with the preoccupation item as primary filter. Administer the preoccupation item once at the start, after consent and before any focal items. Optionally repeat at the end to verify within-survey stability. Do not drop on preoccupation; flag.

- Measure TOT on burn-in items. Insert two burn-in items matched in format to the focal items. Drop respondents below the calibrated floor; do not drop on focal-item TOT.

- Calibrate the TOT floor by mode. When the survey runs across multiple modes (web, phone, face-to-face), calibrate the TOT floor separately within each mode following Holbrook et al. (2003).

- Report quality as part of the deliverable. Filter outcomes, \(\bar D\), the preoccupation distribution, and the burn-in TOT distribution should appear in every client report and academic paper appendix. Side-by-side estimates (full sample vs. flagged-excluded) protect the reader from estimand confusion.

- For sensitive items, layer in social-desirability protection. The literature on sensitive-question methodology (Tourangeau and Smith 1996; Crowne and Marlowe 1960) gives standard tools (item count technique, randomised response, audio computer-assisted self-interview) that reduce social-desirability response bias; intrinsic-stochasticity correction does not substitute for these tools and they do not substitute for it.

- For conjoint experiments, follow the design guidance in Hainmueller et al. (2014) and Bansak et al. (2018). Limit the number of choice tasks per respondent (10–12 is a common upper bound), randomise attribute order, and ensure each forced-choice pair has a within-survey replicate for the Clayton et al. (2025) measurement-error correction.

29.14 Implications for analysis

The instability decomposition has implications downstream of data collection.

29.14.1 Standard errors and effective sample size

If you have used a quality filter, your standard errors should reflect the post-filter sample size, not the recruited sample size. More importantly, if your filter removes respondents non-randomly with respect to the outcome (and almost any non-trivial filter does), your point estimates apply to the filtered population. Be explicit about the change in estimand.

Within-respondent intrinsic stochasticity also reduces effective sample size. With \(\bar D\) and a single administration of the focal item, the variance of the sample mean of the binary outcome is

\[\begin{equation} \mathrm{Var}(\bar Y) \;=\; \frac{p(1-p)}{n_{\text{eff}}},\qquad n_{\text{eff}} \;\le\; n, \tag{29.18} \end{equation}\]

In equation (29.18), \(n_{\text{eff}}\) shrinks as \(\bar D\) rises. The exact relationship depends on the response model, but a useful rule of thumb is \(n_{\text{eff}} \approx n \cdot (1 - 2 \bar D)\) for symmetric misclassification. Power calculations that ignore this overstate power.

29.14.2 Conjoint and discrete-choice analysis

Where AMCEs (average marginal component effects) are reported from forced-choice conjoint experiments (Hainmueller et al. 2014), four additional concerns over and above intrinsic stochasticity now form the standard methodological audit.

- Profile-distribution external validity. Cuesta et al. (2022) show that the AMCE depends critically on the distribution of the non-target attributes used for averaging. A conjoint that randomises attributes uniformly (the field default) generates AMCEs that diverge from real-world choice probabilities when the actual attribute distribution in the target population is highly non-uniform. The remedy is to use the population AMCE (pAMCE), which weights the per-profile contribution by the population distribution of attributes. The

factorExpackage implements both design-based and model-based pAMCE estimators. - Causal interaction beyond the marginal. Egami and Imai (2019) develop the average marginal interaction effect (AMIE) as the proper generalisation of the AMCE to multi-attribute interactions in a factorial design. Unlike the conventional interaction effect, the AMIE does not depend on the choice of baseline conditions, so its sign and magnitude are interpretable even for higher-order interactions.

- Choice-task satisficing. Bansak et al. (2018) test conjoint instruments with up to thirty paired-profile tasks per respondent and find satisficing-induced degradation in recovered AMCEs, although the magnitude is “quite limited.” Their result suggests researchers can administer many tasks without invalidating the design, but the practitioner should still pretest task fatigue at the upper end of any planned task count.

- Within-respondent measurement error. The misclassification-style measurement-error correction in Clayton et al. (2025) should be applied alongside the AMCE/pAMCE/AMIE, using \(\bar D\) from a repeated DV to recover the unattenuated effect. In its absence, AMCEs are biased toward zero, and the bias is non-negligible; Clayton et al. (2025) quantifies the bias as substantial in eight prominent published conjoint analyses. Hainmueller et al. (2015)’s behavioural-validation work on conjoint experiments is the empirical foundation: real-world choice probabilities track conjoint-recovered AMCEs closely, establishing that the conjoint design is informative about real preferences; Clayton et al. (2025) then shows that the within-respondent measurement-error correction tightens that correspondence further.

The four-concern audit (pAMCE, AMIE, satisficing, \(\bar D\) correction) defines the modern minimum-acceptable conjoint analysis.

A closely related stated-preference method that this chapter does not treat in depth, but that deserves mention as a Likert-replacement for many marketing applications, is best-worst scaling (MaxDiff). Respondents see a list of items and choose the best and worst from each subset; the resulting forced-choice data identify a fully ordinal ranking of items with substantially lower response-style contamination than Likert ratings of the same items (Louviere et al. 2015). MaxDiff is now standard in marketing research for attribute-importance estimation and has been demonstrated to reduce extreme-response-style and acquiescence-style bias relative to Likert. For analysts considering a Likert battery on a sensitive or response-style-prone construct, MaxDiff is the preferred alternative.

29.14.3 A closed-form attenuation correction for binary regression