39 Event Studies

The event study methodology is widely used in finance, marketing, and management to measure the impact of specific events on stock prices. The foundation of this methodology is the Efficient Markets Hypothesis proposed by Fama (1970), which asserts that asset prices reflect all available information. Under this assumption, stock prices should immediately react to new, unexpected information, making event studies a useful tool for assessing the economic impact of firm- and non-firm-initiated activities.

A note on descriptive vs. causal interpretation. In its classical finance form, an event study produces a series of abnormal returns: deviations of observed returns from the return predicted by a market (or factor) model. Abnormal returns are a descriptive object. They tell us how prices moved relative to a statistical benchmark around the event window.

Interpreting them as a causal effect of the event on firm value requires additional design-level assumptions:

- The event date is known precisely and was not anticipated. Otherwise the market has priced it in before the window opens.

- No other news or events overlap the event window, so that the price movement is attributable to the focal event and not a confounder.

- The expected-return model is correctly specified during the estimation window.

When these conditions are not met, the event study documents a correlation between a period and a price movement, not a causal effect. In modern empirical practice, event studies are often layered on top of an explicit quasi-experimental design (DiD, RD, or IV): the event-study plot then serves as a visualization of dynamic treatment effects, and the causal identification comes from the underlying design rather than from the event study itself.

A separate and harder question, even granting all three conditions, is whether abnormal returns track the ex-post value created by the event. Section 39.10 reviews the Ben-David et al. (2026) evidence that for corporate acquisitions the answer is essentially no: announcement CAR is uncorrelated with ex-post value-creation measures, and is in fact dominated by news about the standalone acquirer rather than news about the deal. The implication for the rest of this chapter is that “abnormal returns describe a price reaction” and “abnormal returns measure value creation” are two separate empirical claims, and the second requires more than the four foundational assumptions.

The first event study was conducted by Dolley (1933), while Campbell et al. (1998) formalized the methodology for modern applications. Later, Dubow and Monteiro (2006) developed a metric to assess market transparency (i.e., a way to gauge how “clean” a market is) by tracking unusual stock price movements before major regulatory announcements. Their study found that abnormal price shifts before announcements could indicate insider trading, as prices reacted to leaked information before official disclosures.

Advantages of Event Studies

More Reliable than Accounting-Based Measures: Unlike financial metrics (e.g., profits), which managers can manipulate, stock prices are harder to alter and reflect real-time investor sentiment (Benston 1985).

Easy to Conduct: Event studies require only stock price data and simple econometric models, making them widely accessible for researchers.

Types of Events in Event Studies

Table 39.1 groups the events typically analysed by event studies into firm-internal and firm-external categories.

| Event Type | Examples |

|---|---|

| Internal Events | Stock repurchase, earnings announcements, leadership changes |

| External Events | Macroeconomic shocks, regulatory changes, media reports |

39.1 A Brief Tour of How the Method Travelled

It is worth pausing on how the event study became a workhorse in three quite different fields, because the migration from finance into management and then marketing tells you something about what the method actually buys you and what it cannot.

The technique was born in finance. Fama et al. (1969) used the announcement of stock splits to ask a deceptively simple question: do prices adjust to new information immediately, or does adjustment take place over days or weeks? The answer mattered for the efficient-markets hypothesis, but the machinery, pick an event, define a window, compute a normal return, attribute the gap to the event, was general. Once the machinery existed, every field with a clean event and a market response found a use for it.

Management researchers were the next adopters. By the late 1990s the question had shifted from market efficiency to managerial decision-making: do the choices managers make actually create shareholder value, and which ones? McWilliams and Siegel (1997) surveyed how the method had been imported into management research and laid out the methodological cautions, short windows, careful event definition, attention to confounding events, that have shaped practice ever since. Their review remains the standard starting point for anyone applying event studies outside finance.

Marketing scholars adopted the same machinery to defend marketing decisions in the language that boards and CFOs already spoke: stock price. If a brand acquisition, a celebrity endorsement, or a new product launch is supposed to create value, the event study lets us check whether the market thought so on the day the news broke. Two strands of marketing event studies emerged. The first asks about firm-initiated events: things the firm chose to do. The second asks about non-firm-initiated events: things that happened to the firm, often outside its control.

Tables 39.2 and 39.3 collect representative work in each strand, organised by event type so that the table doubles as a reading list for a particular research question. The point is not to memorise these citations but to see the breadth of what an event study can address, from corporate name changes to data breaches, once you accept that “value created” is being proxied by “market reaction”.

| Event Type | Studies |

|---|---|

| Corporate Changes | (Horsky and Swyngedouw 1987) (name change), (Kalaignanam and Bahadir 2013) (corporate brand change) |

| New Product Strategies | (Chaney et al. 1991) (new product announcements), (Raassens et al. 2012) (outsourcing product development), (Sood and Tellis 2009) (innovation payoff), (Borah and Tellis 2014) (make, buy or ally for innovations), (Fang et al. 2015) (co-development agreements) |

| Brand & Marketing Strategies | (Lane and Jacobson 1995) (brand extensions), (Wiles et al. 2012) (brand acquisition) |

| Advertising & Promotions | (Wiles et al. 2010) (deceptive advertising), (Cornwell et al. 2005) (sponsorship announcements) |

| Strategic Alliances | (Houston and Johnson 2000) (joint ventures), (Fang et al. 2015) (co-development agreements), (Sorescu et al. 2007) (M&A), (Homburg et al. 2014) (channel expansions) |

| Entertainment & Celebrity Endorsements | (Agrawal and Kamakura 1995) (celebrity endorsements), (Elberse 2007) (casting announcements), (Wiles and Danielova 2009) (product placement in movies), (Joshi and Hanssens 2009) (movie releases), (Karniouchina et al. 2011) (product placement), (Mazodier and Rezaee 2013) (sports announcements) |

Two further marketing studies sit slightly outside that grid but illustrate the same logic: Geyskens et al. (2002) examined newspapers’ decisions to launch internet channels, and Boyd et al. (2010) looked at the market’s reaction to new CMO appointments. Both treat a strategic choice as the event and ask whether shareholders rewarded or punished it.

The non-firm-initiated literature is structurally similar but methodologically more demanding. Because the firm did not choose the event, the researcher has fewer levers to manipulate: there is no internal documentation of the announcement timing, leakage is harder to rule out, and selection into “events that journalists write about” is itself a research question. The studies in Table 39.3 tackle this in different ways, some focus on regulator-announced events with a clean publication date, others on negative shocks where the firm’s response is partly endogenous to the event itself.

| Event Type | Studies |

|---|---|

| Regulatory Decisions | (Sorescu et al. 2003) (FDA approvals), (Rao et al. 2008) (FDA approvals), (Tipton et al. 2009) (deceptive advertising regulation) |

| Media Coverage & Consumer Reactions | (Jacobson and Mizik 2009) (customer satisfaction score release), (Chen et al. 2012) (third-party movie reviews), (Tellis and Johnson 2007) (quality reviews by Walter Mossberg) |

| Economic & Market Shocks | (Gielens et al. 2008) (Walmart’s entry into the UK), (Xiong and Bharadwaj 2013) (asymmetric news impact), (Pandey et al. 2005) (diversity elite list) |

| Consumer & Industry Recognitions | (Balasubramanian et al. 2005) (high-quality achievements), (Fornell et al. 2006) (customer satisfaction), (Ittner et al. 2009) (customer satisfaction) |

| Financial & Market Reactions | (Boyd and Spekman 2008) (indirect ties), (Karniouchina et al. 2009) (Mad Money with Jim Cramer), (Bhagat et al. 1998) (litigation) |

| Product & Service Failures | (Y. Chen et al. 2009) (product recalls), (Gao et al. 2015) (product recalls), (Malhotra and Kubowicz Malhotra 2011) (data breach) |

The space of plausible event studies is far from exhausted. Major advertising campaigns, market entries, product recalls, and patent announcements are all candidate events whose informational content arrives with a clean timestamp and whose effect on firm value is in principle measurable. Whenever you encounter a setting where (a) the event is dated precisely, (b) market participants could plausibly update on it, and (c) you can construct a defensible counterfactual from the estimation window, the apparatus that follows in this chapter is in scope.

39.2 Key Assumptions

The interpretation of an event study, whether descriptive or causal, rests on a small set of assumptions about how prices, information, and the firm’s stakeholders interact. None of these are testable in the strong sense that randomization is, and each fails in identifiable ways. Reading the four assumptions below as licensing claims, each one buying you a specific interpretation, is more useful than reading them as a checklist.

The Efficient Market Hypothesis (Fama 1970) is the load-bearing assumption. It says that stock prices fully and instantly reflect publicly available information, so a measurable price reaction in the days surrounding an event is interpretable as the market’s revaluation of the firm in light of the event’s news content. When EMH holds in its strong form, the event window is exactly where the news shows up; when it holds only weakly (information leaks before the announcement, prices drift in the days after), the analyst must widen the window or accept that the estimated abnormal return is contaminated. EMH is not all-or-nothing in practice, and most modern event studies assume a semi-strong form (prices reflect public information) rather than a strong form (prices reflect all information including private signals).

The stock market as a proxy for firm value assumption says that the price of equity is a meaningful summary of the firm’s value to its primary stakeholders. This is uncontroversial in finance applications where shareholders are the relevant audience. It is more contested in marketing or management applications, where the relevant audience is sometimes customers, employees, or regulators, and where firm value to those stakeholders is not perfectly tracked by share prices. The closer the research question is to “what did this event do to shareholder wealth?”, the better this assumption holds; the further it is from that question, the more the analyst should report alternative outcome measures alongside abnormal returns.

The sharp event-effect assumption requires that the event causes an immediate and concentrated price reaction. If the market reacts gradually over several months, no plausible event window will isolate the effect; if the market anticipates the event, the price has already moved before the window opens. The assumption is most credible for events with precise timestamps that the market could not have anticipated (regulatory rulings on a fixed announcement date, court verdicts, corporate disclosures with mandated reporting calendars). It is least credible for events whose probability of occurrence was already partially priced in, in which case the abnormal return measures the surprise component, not the full effect of the event.

The proper calculation of expected returns is what gives the abnormal return a benchmark. The mechanics matter: a market model with the wrong factor specification, an estimation window that includes a structural break, or a beta estimated on a thin sample will all produce expected returns that misstate the counterfactual price path. The downstream consequence is that the abnormal return is only as clean as the expected-return model. We return to this point in the expected return calculation section and the econometric event-study designs section.

These four assumptions together support a descriptive claim, that the abnormal return measures the price reaction to the event window. Promoting that descriptive claim to a causal claim, that the event itself caused the price reaction, requires the additional design-level assumptions discussed at the start of this chapter: no contemporaneous confounding events, no anticipation, and a benchmark model that is correctly specified throughout the estimation window. Modern empirical practice typically pairs the event-study machinery with an explicit quasi-experimental design (Regression Discontinuity, examiner IV, or Difference-in-Differences) so that the causal claim does not rest on the four assumptions above alone.

39.3 Steps for Conducting an Event Study

39.3.1 Step 1: Event Identification

An event study examines how a particular event affects a firm’s stock price, assuming that stock markets incorporate new information efficiently. The event must influence either the firm’s expected cash flows or discount rate (Sorescu et al. 2017, 191).

Common Types of Events Analyzed

Table 39.4 lists the broad event categories most often analysed and gives concrete examples of each.

| Event Category | Examples |

|---|---|

| Corporate Actions | Dividends, mergers & acquisitions (M&A), stock buybacks, name changes, brand extensions, sponsorships, product launches, advertising campaigns |

| Regulatory Changes | New laws, taxation policies, financial deregulation, trade agreements |

| Market Events | Privatization, nationalization, entry/exit from major indices |

| Marketing-Related Events | Celebrity endorsements, new product announcements, media reviews |

| Crisis & Negative Shocks | Product recalls, data breaches, lawsuits, financial fraud scandals |

To systematically identify events, researchers use WRDS S&P Capital IQ Key Developments, which tracks U.S. and international corporate events.

39.3.2 Step 2: Define the Event and Estimation Windows

39.3.2.1 (A) Estimation Window (\(T_0 \to T_1\))

The estimation window is used to compute normal (expected) returns before the event. Table 39.5 summarises common choices in the literature.

| Study | Estimation Window |

|---|---|

| (Johnston 2007) | 250 days before the event, with a 45-day gap before the event window |

| (Wiles et al. 2012) | 90-trading-day estimation window ending 6 days before the event |

| (Sorescu et al. 2017, 194) | 100 days before the event |

Leakage Concern: To avoid biases from information leaking before the event, researchers should check broad news sources (e.g., LexisNexis, Factiva, RavenPack) for pre-event rumors.

39.3.2.2 (B) Event Window (\(T_1 \to T_2\))

The event window captures the market’s reaction to the event. The selection of an appropriate window length depends on event type and information speed; Table 39.6 reports choices used in the literature.

| Study | Event Window |

|---|---|

| (Balasubramanian et al. 2005; Boyd et al. 2010; Fornell et al. 2006) | 1-day window |

| (Raassens et al. 2012; Sood and Tellis 2009) | 2-day window |

| (Cornwell et al. 2005; Sorescu et al. 2007) | Up to 10 days |

39.3.3 Step 3: Compute Normal vs. Abnormal Returns

The abnormal return measures how much the stock price deviates from its expected return:

\[ \text{AR}_{it} = R_{it} - E(R_{it} \mid X_t) \]

where:

\(\text{AR}_{it}\) = abnormal return for firm \(i\) at time \(t\)

\(R_{it}\) = realized (dividend-adjusted) return

\(E(R_{it} \mid X_t)\) = expected return given the conditioning information \(X_t\) (typically the market or factor returns over the estimation window)

39.3.3.1 (A) Statistical Models for Expected Returns

These models assume jointly normal and independently distributed returns.

-

Constant Mean Return Model

\[ E(R_{it}) = \frac{1}{T} \sum_{t=T_0}^{T_1} R_{it} \] -

Market Model

\[ R_{it} = \alpha_i + \beta_i R_{mt} + \epsilon_{it} \] -

Adjusted Market Return Model

\[ E(R_{it}) = R_{mt} \]

39.3.4 Step 4: Compute Cumulative Abnormal Returns

Once abnormal returns are computed, we aggregate them over the event window:

\[ CAR_{i} = \sum_{t=T_{\text{event, start}}}^{T_{\text{event, end}}} AR_{it} \]

For multiple firms, compute the Average Cumulative Abnormal Return (ACAR):

\[ ACAR = \frac{1}{N} \sum_{i=1}^{N} CAR_{i} \]

39.4 Event Studies in Marketing

A key challenge in marketing-related event studies is determining the appropriate dependent variable (Skiera et al. 2017). Traditional event studies in finance use cumulative abnormal returns (CAR) on shareholder value (\(CAR^{SHV}\)). However, marketing events primarily affect a firm’s operating business, rather than its total shareholder value, leading to potential distortions if financial leverage is ignored.

According to valuation theory, a firm’s shareholder value (\(SHV\)) consists of three components (Schulze et al. 2012):

\[ SHV = \text{Operating Business Value} + \text{Non-Operating Assets} - \text{Debt} \]

Many marketing-related events primarily impact operating business value (e.g., brand perception, customer satisfaction, advertising efficiency), while non-operating assets and debt remain largely unaffected.

Ignoring firm-specific leverage effects in event studies can cause:

- Inflated impact for firms with high debt.

- Deflated impact for firms with large non-operating assets.

Thus, it is recommended that both \(CAR^{OB}\) and \(CAR^{SHV}\) be reported, with justification for which is most appropriate.

Surprisingly few event studies have explicitly controlled for financial structure. Two exceptions are worth flagging because they show how the correction can be operationalised. Chaney et al. (1991) look at the relationship between advertising expenses and firm value while explicitly holding leverage in the picture, and Gielens et al. (2008) extend the same logic to marketing-spending shocks. Outside this small literature, the implicit assumption is that leverage is uncorrelated with the event of interest, which is rarely defended and often demonstrably false.

39.4.1 Definition

- Cumulative Abnormal Return on Shareholder Value (\(CAR^{SHV}\))

\[ CAR^{SHV} = \frac{\sum \text{Abnormal Returns}}{SHV} \]

-

Shareholder Value (\(SHV\)): Market capitalization, defined as:

\[ SHV = \text{Share Price} \times \text{Shares Outstanding} \]

- Cumulative Abnormal Return on Operating Business (\(CAR^{OB}\))

To correct for leverage effects, \(CAR^{OB}\) is calculated as:

\[ CAR^{OB} = \frac{CAR^{SHV}}{\text{Leverage Effect}} \]

where:

\[ \text{Leverage Effect} = \frac{\text{Operating Business Value}}{\text{Shareholder Value}} \]

Key Relationships:

- Operating Business Value = \(SHV -\) Non-Operating Assets \(+\) Debt.

- Leverage Effect (\(LE\)) measures how a 1% change in operating business value translates into shareholder value movement.

- Leverage Effect vs. Leverage Ratio

Leverage Effect (\(LE\)) is not the same as the leverage ratio, which is typically:

\[ \text{Leverage Ratio} = \frac{\text{Debt}}{\text{Firm Size}} \]

where firm size can be:

Book value of equity

Market capitalization

Total assets

Debt + Equity

39.4.2 When Can Marketing Events Affect Non-Operating Assets or Debt?

While most marketing events impact operating business value, in rare cases they also influence non-operating assets and debt (Table 39.7).

| Marketing Event | Impact on Financial Structure |

|---|---|

| Excess Pre-ordering (Hall et al. 2004) | Affects short-term debt |

| CMO Turnover (Berger et al. 1997) | Higher debt due to manager turnover |

| Unique Product Development (Bhaduri 2002) | Alters debt levels |

These exceptions highlight why controlling for financial structure is crucial in event studies.

39.4.3 Calculating the Leverage Effect

We can express leverage effect (\(LE\)) as:

\[ \begin{aligned} LE &= \frac{\text{Operating Business Value}}{\text{Shareholder Value}} \\ &= \frac{(\text{SHV} - \text{Non-Operating Assets} + \text{Debt})}{\text{SHV}} \\ &= \frac{prcc_f \times csho - ivst + dd1 + dltt + pstk}{prcc_f \times csho} \end{aligned} \]

where:

\(prcc_f\) = Share price

\(csho\) = Common shares outstanding

\(ivst\) = Short-term investments (Non-Operating Assets)

\(dd1\) = Long-term debt due in one year

\(dltt\) = Long-term debt

\(pstk\) = Preferred stock

39.4.4 Computing Leverage Effect from Compustat Data

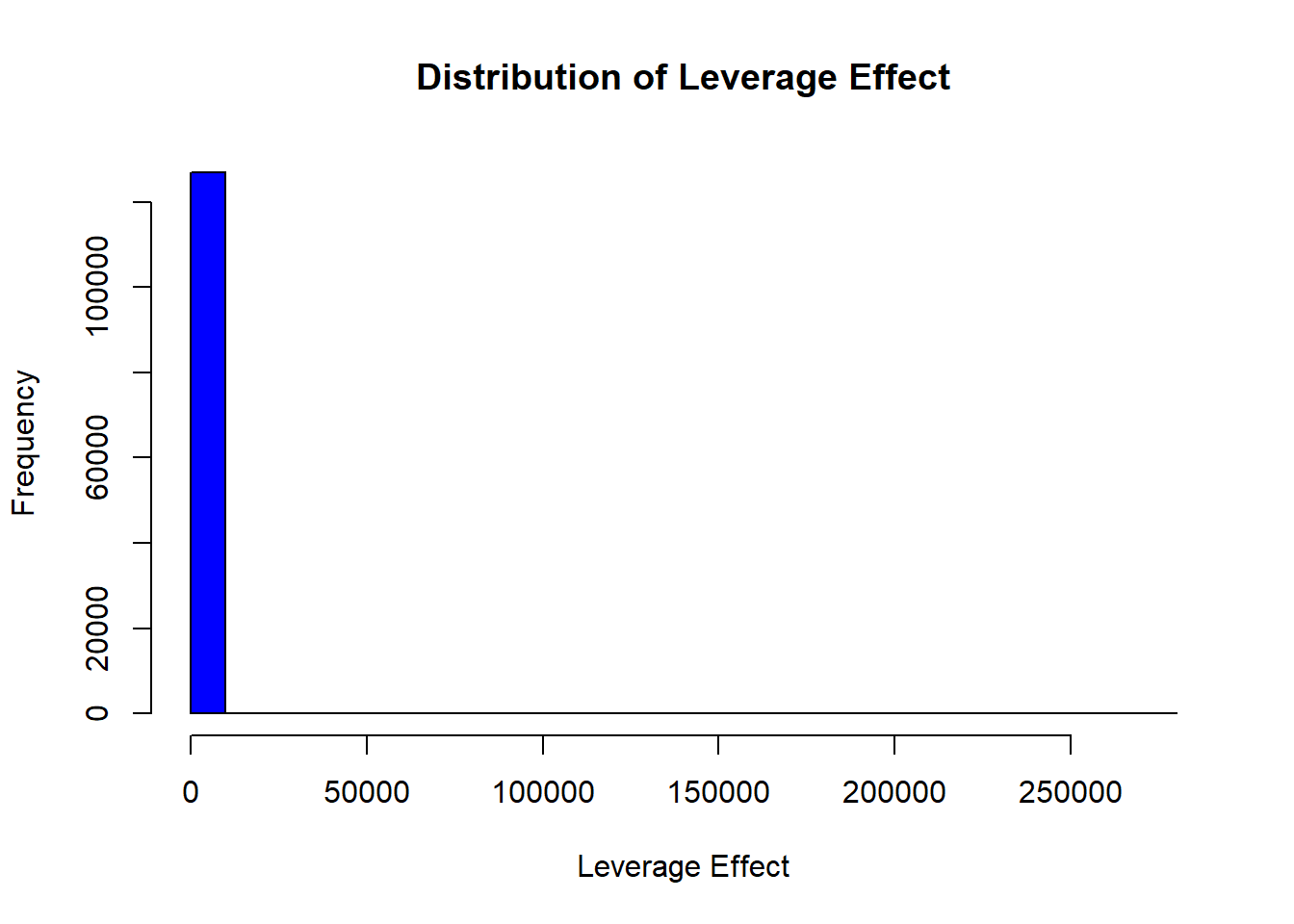

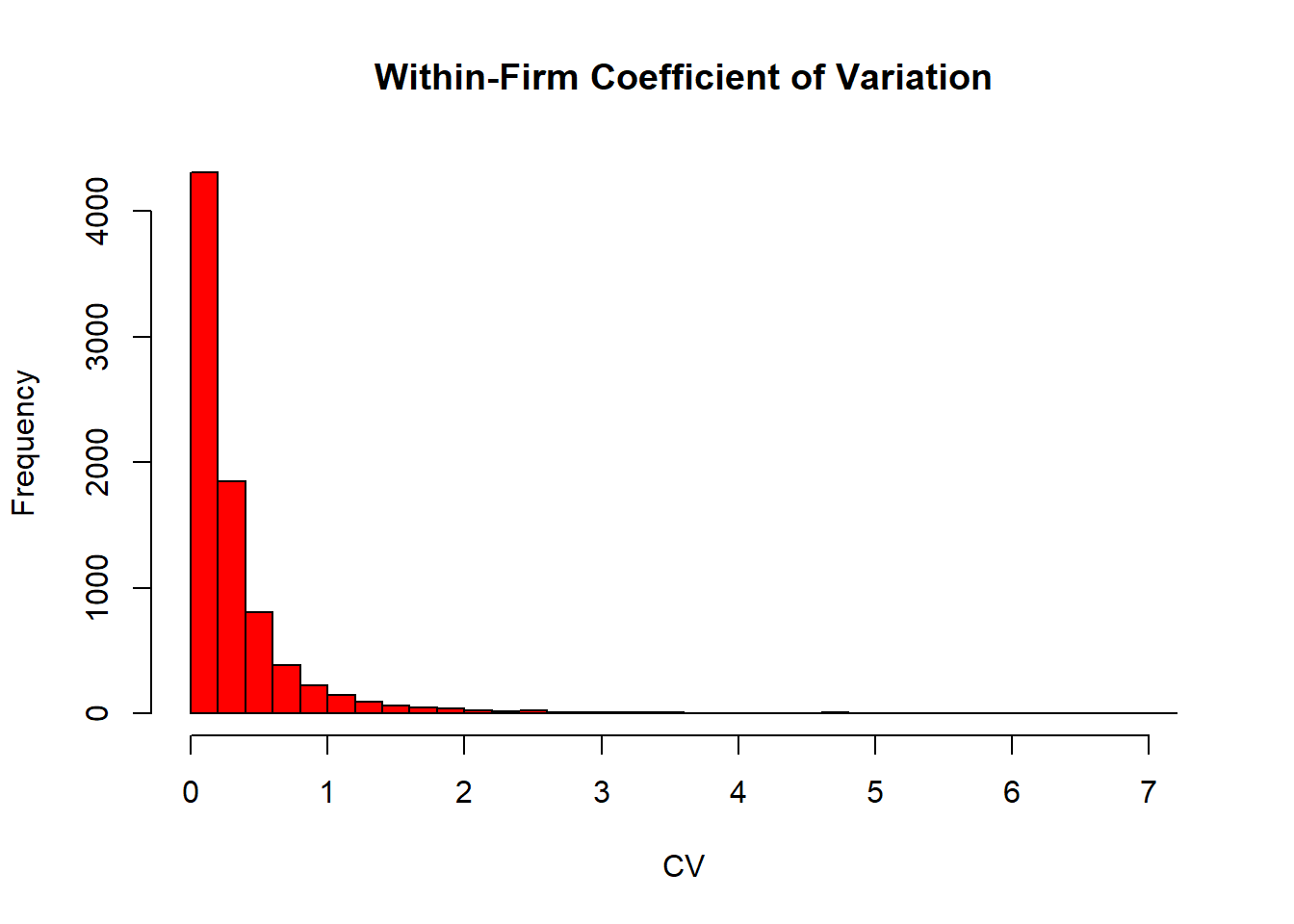

The code below computes and visualizes the cross-firm distribution of the leverage effect from Compustat together with the within-firm coefficient of variation across years.

# Load required libraries

library(tidyverse)

# Load dataset

df_leverage_effect <- read.csv("data/leverage_effect.csv.gz") %>%

# Filter active firms

filter(costat == "A") %>%

# Drop missing values

drop_na() %>%

# Compute Shareholder Value (SHV)

mutate(shv = prcc_f * csho) %>%

# Compute Operating Business Value (OBV)

mutate(obv = shv - ivst + dd1 + dltt + pstk) %>%

# Compute Leverage Effect

mutate(leverage_effect = obv / shv) %>%

# Remove infinite values and non-positive leverage effects

filter(is.finite(leverage_effect), leverage_effect > 0) %>%

# Compute within-firm statistics

group_by(gvkey) %>%

mutate(

within_mean_le = mean(leverage_effect, na.rm = TRUE),

within_sd_le = sd(leverage_effect, na.rm = TRUE)

) %>%

ungroup()

# Summary statistics

mean_le <- mean(df_leverage_effect$leverage_effect, na.rm = TRUE)

max_le <- max(df_leverage_effect$leverage_effect, na.rm = TRUE)

# Plot histogram of leverage effect

hist(

df_leverage_effect$leverage_effect,

main = "Distribution of Leverage Effect",

xlab = "Leverage Effect",

col = "blue",

breaks = 30

)

# Compute coefficient of variation (CV)

cv_le <-

sd(df_leverage_effect$leverage_effect, na.rm = TRUE) / mean_le * 100

# Plot within-firm coefficient of variation histogram

df_leverage_effect %>%

group_by(gvkey) %>%

slice(1) %>%

ungroup() %>%

mutate(cv = within_sd_le / within_mean_le) %>%

pull(cv) %>%

hist(

main = "Within-Firm Coefficient of Variation",

xlab = "CV",

col = "red",

breaks = 30

)

39.5 Economic Significance

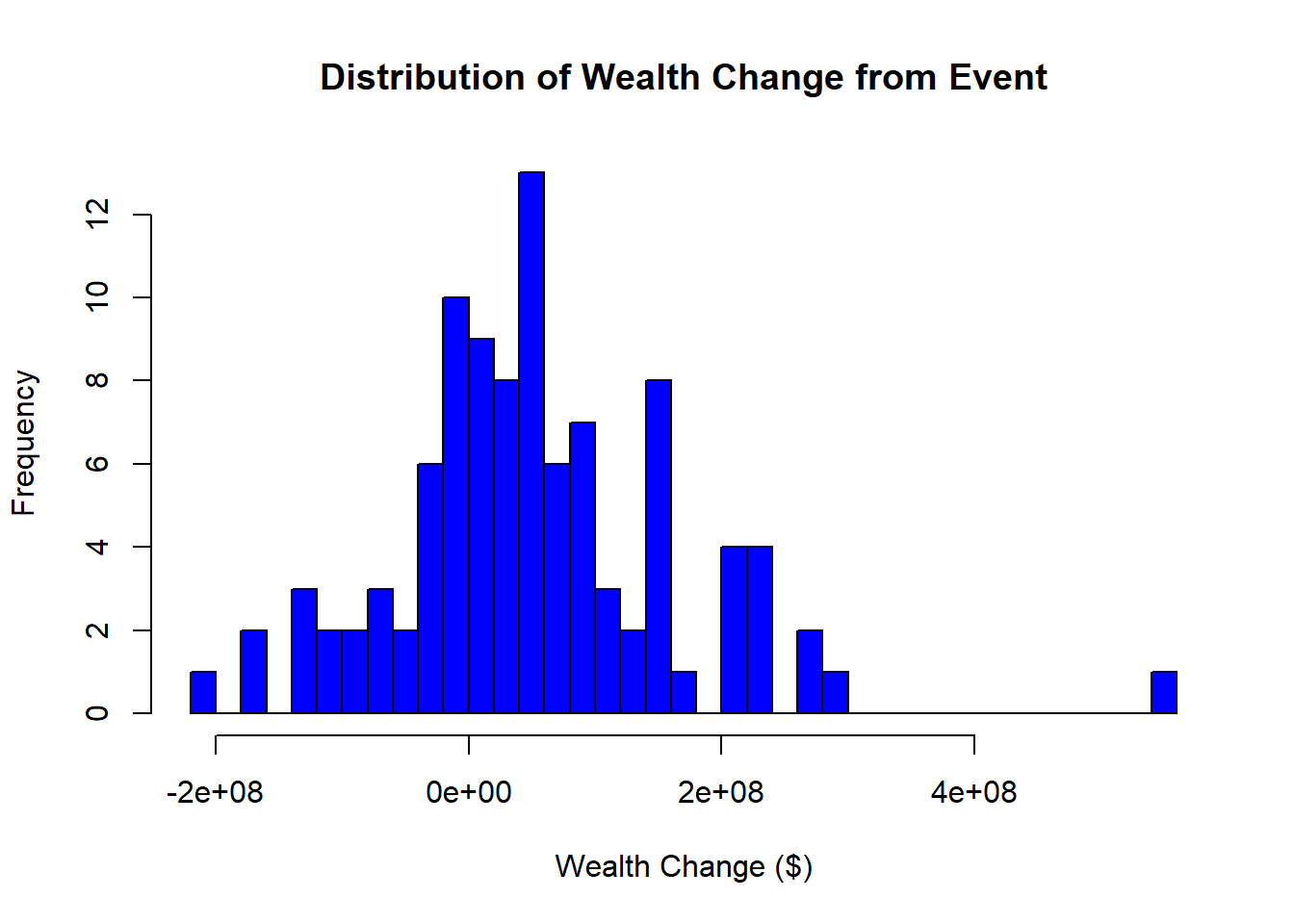

The total wealth gain (or loss) resulting from a marketing event is given by:

\[ \Delta W_t = CAR_t \times MKTVAL_0 \]

where:

- \(\Delta W_t\) = Change in firm value (gain or loss).

- \(CAR_t\) = Cumulative abnormal return up to date \(t\).

- \(MKTVAL_0\) = Market value of the firm before the event window.

Interpretation:

- If \(\Delta W_t > 0\): The event increased firm value.

- If \(\Delta W_t < 0\): The event decreased firm value.

- The magnitude of \(\Delta W_t\) reflects the economic impact of the marketing event in dollar terms.

By computing \(\Delta W_t\), researchers can translate stock market reactions into tangible financial implications, helping assess the real-world significance of marketing decisions.

Figure 39.1 shows the simulated distribution of dollar wealth change \(\Delta W_t\) across 100 firms drawn from a normal CAR distribution and a uniform pre-event market value.

# Load necessary libraries

library(tidyverse)

# Simulated dataset of event study results

df_event_study <- tibble(

firm_id = 1:100,

# 100 firms

CAR_t = rnorm(100, mean = 0.02, sd = 0.05),

# Simulated CAR values

MKTVAL_0 = runif(100, min = 1e8, max = 5e9) # Market value in dollars

)

# Compute total wealth gain/loss

df_event_study <- df_event_study %>%

mutate(wealth_change = CAR_t * MKTVAL_0)

# Summary statistics of economic impact

summary(df_event_study$wealth_change)

#> Min. 1st Qu. Median Mean 3rd Qu. Max.

#> -231887493 -36267464 36156060 61726671 160218303 538036037

# Histogram of total wealth gain/loss

hist(

df_event_study$wealth_change,

main = "Distribution of Wealth Change from Event",

xlab = "Wealth Change ($)",

col = "blue",

breaks = 30

)

Figure 39.1: Distribution of simulated dollar wealth change from a marketing event across 100 firms, computed as CAR times pre-event market value.

39.6 Testing in Event Studies

39.6.1 Statistical Power in Event Studies

Statistical power refers to the ability to detect a true effect (i.e., identify significant abnormal returns) when one exists.

Power increases with:

- More firms in the sample → reduces variance and increases reliability.

- Fewer days in the event window → avoids contamination from other confounding factors.

Trade-Off:

- A longer event window captures delayed market reactions but risks contamination from unrelated events.

- A shorter event window reduces noise but may miss slow adjustments in stock prices.

Thus, an optimal event window balances precision (avoiding confounds) and completeness (capturing true market reaction).

39.6.2 Parametric Tests

Brown and Warner (1985) provide evidence that parametric tests perform well even under non-normality, as long as the sample includes at least five securities. This is because the distribution of abnormal returns converges to normality as the sample size increases.

39.6.2.1 Power of Parametric Tests

Kothari and Warner (1997) highlights that the power to detect significant abnormal returns depends on:

- Sample size: More firms improve statistical power.

- Magnitude of abnormal returns: Larger effects are easier to detect.

- Variance of abnormal returns across firms: Lower variance increases power.

39.6.2.2 T-Test for Abnormal Returns

By applying the Central Limit Theorem, we can use the t-test for abnormal returns:

\[ \begin{aligned} t_{CAR} &= \frac{\overline{CAR_{it}}}{\sigma (CAR_{it})/\sqrt{n}} \\ t_{BHAR} &= \frac{\overline{BHAR_{it}}}{\sigma (BHAR_{it})/\sqrt{n}} \end{aligned} \]

Assumptions:

Abnormal returns follow a normal distribution.

Variance is equal across firms.

No cross-sectional correlation in abnormal returns.

If these assumptions do not hold, the t-test will be misspecified, leading to unreliable inference.

Misspecification may occur due to:

Heteroskedasticity (unequal variance across firms).

Cross-sectional dependence (correlation in abnormal returns across firms).

Non-normality of abnormal returns (though event study design often forces normality).

To address these concerns, Patell Standardized Residuals provide a robust alternative.

39.6.2.3 Patell Standardized Residual

Patell (1976) developed the Patell Standardized Residuals (PSR), which standardizes abnormal returns to correct for estimation errors.

Since the market model relies on observations outside the event window, it introduces prediction errors beyond true residuals. PSR corrects for this:

\[ AR_{it} = \frac{\hat{u}_{it}}{s_i \sqrt{C_{it}}} \]

where:

- \(\hat{u}_{it}\) = estimated residual from the market model.

- \(s_i\) = standard deviation of residuals from the estimation period.

- \(C_{it}\) = correction factor accounting for estimation period variation.

The correction factor (\(C_{it}\)) is:

\[ C_{it} = 1 + \frac{1}{T} + \frac{(R_{mt} - \bar{R}_m)^2}{\sum_t (R_{mt} - \bar{R}_m)^2} \]

where:

- \(T\) = number of observations in the estimation period.

- \(R_{mt}\) = market return at time \(t\).

- \(\bar{R}_m\) = mean market return.

This correction ensures abnormal returns are properly scaled, reducing bias from estimation errors.

39.6.2.4 Boehmer-Musumeci-Poulsen Standardized Cross-Sectional Test

The Patell test corrects for prediction error in the estimation window but assumes the event-window variance equals the estimation-window variance. That assumption fails whenever the event itself perturbs return volatility, which is the norm rather than the exception: corporate-action announcements, regulatory shocks, and major news releases all tend to widen the cross-section of returns on the announcement date relative to ordinary trading days. Boehmer et al. (1991) show that ignoring this event-induced variance causes the Patell test to reject the null too often, sometimes dramatically so, and propose a standardized cross-sectional statistic that absorbs the shift. The BMP test divides each firm’s Patell-standardized abnormal return by the cross-sectional standard deviation of those standardized returns within the event window, so any common increase in variance is differenced out. In simulation studies and empirical comparisons it has displaced Patell as the default short-window test for any sample where the event might plausibly shift variance, which is almost all of them.

Harrington and Shrider (2007) extend the logic one step further by showing analytically that any cross-sectional heterogeneity in event effects, not just an aggregate variance shift, mechanically inflates event-window variance relative to the estimation window. Their recommendation, which is now standard, is to use BMP-style tests as the default even when no aggregate variance shift is suspected, because firm-level heterogeneity in the underlying effect is virtually unavoidable in real samples.

39.6.2.5 Kolari-Pynnonen Adjusted Tests for Cross-Sectional Correlation

BMP corrects for event-induced variance but still treats abnormal returns as independent across firms. When events cluster in calendar time, as they routinely do for sector regulations, market-wide announcements, or industry shocks, abnormal returns across firms share a common factor that the independence assumption ignores. Kolari and Pynnönen (2010) show that this cross-sectional correlation biases the BMP statistic upward and propose a one-line correction: multiply the BMP statistic by \(\sqrt{(1 - \bar{r}) / (1 + (n-1) \bar{r})}\), where \(\bar{r}\) is the average pairwise correlation of estimation-window residuals across the \(n\) sample firms. The adjusted statistic, often labeled ADJ-BMP or the Kolari-Pynnonen test, restores correct rejection rates in clustered-event samples and reduces to BMP exactly when residuals are uncorrelated.

Kolari and Pynnönen (2011) provide a companion generalized rank test (GRANK) that is simultaneously robust to event-induced volatility, cross-sectional correlation, and non-normality, making it the most defensible nonparametric default for short-window studies. The progression Patell to BMP to ADJ-BMP/GRANK now defines best-practice inference: pick the test whose robustness profile matches the threats present in the sample, and report results across multiple tests when they disagree.

39.6.2.6 Contaminated Estimation Windows

A subtler inferential problem arises when the estimation window itself is dirty. Serial acquirers, repeat issuers, or firms in industries with frequent news flow violate the implicit assumption that the estimation window contains only “normal” return generation. Aktas et al. (2007) document the bias this introduces, larger and more variable abnormal returns than the true effect, and propose a two-state market-model adjustment that downweights estimation-window observations contaminated by other firm-specific news. The fix is most consequential for samples of serial acquirers and for firms in M&A-active industries, where the convention of fitting the market model on the most recent 250 days routinely overlaps other event windows.

39.6.3 Non-Parametric Tests

Non-parametric tests do not assume a specific return distribution, making them robust to non-normality and heteroskedasticity.

39.6.3.1 Sign Test

The Sign Test assumes symmetric abnormal returns around zero.

- Null hypothesis (\(H_0\)): Equal probability of positive and negative abnormal returns.

- Alternative hypothesis (\(H_A\)): More positive (or negative) abnormal returns than expected.

# Perform a sign test using binomial test

binom.test(x = sum(CAR > 0), n = length(CAR), p = 0.5)39.6.3.2 Wilcoxon Signed-Rank Test

The Wilcoxon Signed-Rank Test allows for non-symmetry in returns.

Use case: Detects shifts in the distribution of abnormal returns.

More powerful than the sign test when return magnitudes matter.

# Perform Wilcoxon Signed-Rank Test

wilcox.test(CAR, mu = 0)39.6.3.3 Generalized Sign Test

A more advanced sign test, comparing the proportion of positive abnormal returns to historical norms, proposed by Cowan (1992).

39.6.3.4 Corrado Rank Test

The Corrado Rank Test (Corrado 1989) is a rank-based test for abnormal returns.

Advantage: Accounts for cross-sectional dependence.

More robust than the t-test under non-normality.

# Load necessary libraries

library(tidyverse)

# Simulate abnormal returns (CAR)

set.seed(123)

df_returns <- tibble(

firm_id = 1:100, # 100 firms

CAR = rnorm(100, mean = 0.02, sd = 0.05) # Simulated CAR values

)

# Parametric T-Test for CAR

t_test_result <- t.test(df_returns$CAR, mu = 0)

# Non-parametric tests

sign_test_result <- binom.test(sum(df_returns$CAR > 0), n = nrow(df_returns), p = 0.5)

wilcox_test_result <- wilcox.test(df_returns$CAR, mu = 0)

# Print results

list(

T_Test = t_test_result,

Sign_Test = sign_test_result,

Wilcoxon_Test = wilcox_test_result

)

#> $T_Test

#>

#> One Sample t-test

#>

#> data: df_returns$CAR

#> t = 5.3725, df = 99, p-value = 5.159e-07

#> alternative hypothesis: true mean is not equal to 0

#> 95 percent confidence interval:

#> 0.01546417 0.03357642

#> sample estimates:

#> mean of x

#> 0.0245203

#>

#>

#> $Sign_Test

#>

#> Exact binomial test

#>

#> data: sum(df_returns$CAR > 0) and nrow(df_returns)

#> number of successes = 70, number of trials = 100, p-value = 7.85e-05

#> alternative hypothesis: true probability of success is not equal to 0.5

#> 95 percent confidence interval:

#> 0.6001853 0.7875936

#> sample estimates:

#> probability of success

#> 0.7

#>

#>

#> $Wilcoxon_Test

#>

#> Wilcoxon signed rank test with continuity correction

#>

#> data: df_returns$CAR

#> V = 3917, p-value = 1.715e-06

#> alternative hypothesis: true location is not equal to 039.7 Sample in Event Studies

A practical question that often surprises newcomers to event studies is how few observations are typically involved. Marketing and finance applications routinely run on samples that would look anaemic in other empirical traditions, and yet they regularly yield publishable, interpretable results. A glance at the published record gives a sense of the range. Markovitch and Golder (2008) work with 71 events at the small end of the distribution; Wiles et al. (2012) have a more typical setup with 572 acquisition announcements and 308 disposal announcements; Borah and Tellis (2014) sit at the upper end with 3,552 events. The lesson is not that sample size doesn’t matter, larger samples buy more power and tighter inference, but that the signal in an event study comes from the sharpness of the event window relative to normal-return variation, not from raw \(N\). With clean events and a well-specified normal-return model, a few dozen carefully curated cases can yield results that would survive in a much larger study with noisier identification.

39.8 Confounders in Event Studies

A major challenge in event studies is controlling for confounding events, which could bias the estimation of abnormal returns.

39.8.1 Types of Confounding Events

(McWilliams and Siegel 1997) suggest excluding firms that experience other major events within a two-day window around the focal event. These include:

- Financial announcements: Earnings reports, stock buybacks, dividend changes, IPOs.

- Corporate actions: Mergers, acquisitions, spin-offs, stock splits, debt defaults.

- Executive changes: CEO/CFO resignations or appointments.

- Operational changes: Layoffs, restructurings, lawsuits, joint ventures.

Fornell et al. (2006) recommend:

- One-day event period: The date when Wall Street Journal publishes the ACSI announcement.

- Five-day window (before and after the event) to rule out other news (from PR Newswires, Dow Jones, Business Wires).

Events controlled for include:

M&A, spin-offs, stock splits.

CEO or CFO changes.

Layoffs, restructurings, lawsuits.

A useful data source for identifying confounding events is Capital IQ’s Key Developments, which captures almost all important corporate events.

39.8.2 Should We Exclude Confounded Observations?

Sorescu et al. (2017) investigated confounding events in short-term event windows using:

RavenPack dataset (2000-2013).

3-day event windows for 3,982 US publicly traded firms.

Key Findings:

- The difference between the full sample and the sample without confounded events was statistically insignificant.

- Conclusion: Excluding confounded observations may not be necessary in short-term event studies.

Why?

- Selection bias risk: Researchers may selectively exclude events, introducing bias.

- Increasing exclusions over time: As time progresses, more events need to be excluded, reducing statistical power.

- Short-term windows minimize confounder effects.

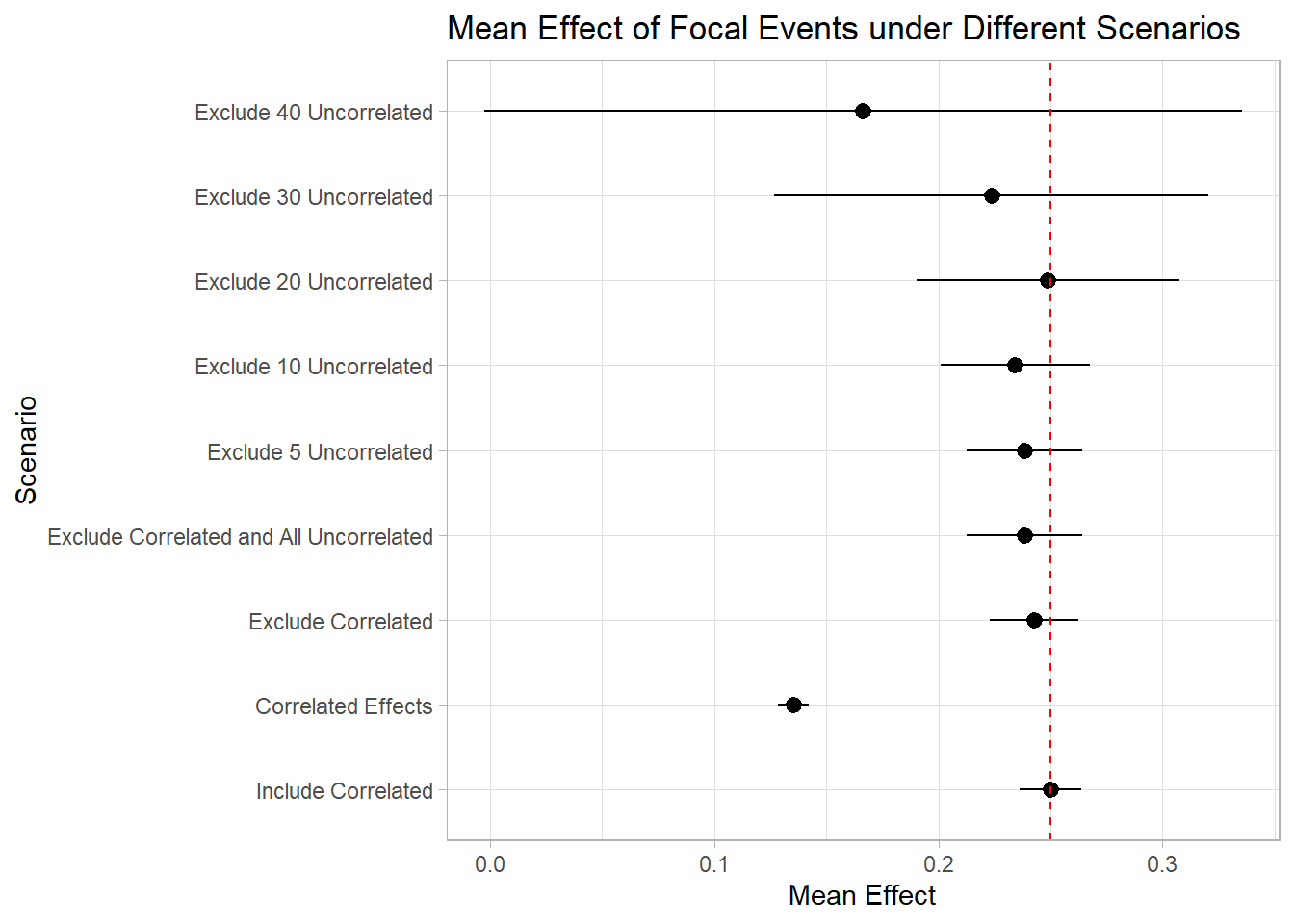

39.8.3 Simulation Study: Should We Exclude Correlated and Uncorrelated Events?

To illustrate the impact of correlated and uncorrelated events, let’s conduct a simulation study.

We consider three event types:

- Focal events (events of interest).

- Correlated events (events that often co-occur with focal events).

- Uncorrelated events (random events that might coincide with focal events).

We will analyze the impact of including vs. excluding correlated and uncorrelated events.

Figure 39.2 plots the estimated mean focal-event effect, with 95% confidence intervals, under scenarios that progressively include or exclude correlated and uncorrelated events.

# Load required libraries

library(dplyr)

library(ggplot2)

library(tidyr)

library(tidyverse)

# Parameters

n <- 100000 # Number of observations

n_focal <- round(n * 0.2) # Number of focal events

overlap_correlated <- 0.5 # Overlapping percentage between focal and correlated events

# Function to compute mean and confidence interval

mean_ci <- function(x) {

m <- mean(x)

ci <- qt(0.975, length(x)-1) * sd(x) / sqrt(length(x)) # 95% confidence interval

list(mean = m, lower = m - ci, upper = m + ci)

}

# Simulate data

set.seed(42)

data <- tibble(

date = seq.Date(

from = as.Date("2010-01-01"),

by = "day",

length.out = n

),

# Date sequence

focal = rep(0, n),

correlated = rep(0, n),

ab_ret = rnorm(n)

)

# Define focal events

focal_idx <- sample(1:n, n_focal)

data$focal[focal_idx] <- 1

true_effect <- 0.25

# Adjust the ab_ret for the focal events to have a mean of true_effect

data$ab_ret[focal_idx] <-

data$ab_ret[focal_idx] - mean(data$ab_ret[focal_idx]) + true_effect

# Determine the number of correlated events that overlap with focal and those that don't

n_correlated_overlap <-

round(length(focal_idx) * overlap_correlated)

n_correlated_non_overlap <- n_correlated_overlap

# Sample the overlapping correlated events from the focal indices

correlated_idx <- sample(focal_idx, size = n_correlated_overlap)

# Get the remaining indices that are not part of focal

remaining_idx <- setdiff(1:n, focal_idx)

# Check to ensure that we're not attempting to sample more than the available remaining indices

if (length(remaining_idx) < n_correlated_non_overlap) {

stop("Not enough remaining indices for non-overlapping correlated events")

}

# Sample the non-overlapping correlated events from the remaining indices

correlated_non_focal_idx <-

sample(remaining_idx, size = n_correlated_non_overlap)

# Combine the two to get all correlated indices

all_correlated_idx <- c(correlated_idx, correlated_non_focal_idx)

# Set the correlated events in the data

data$correlated[all_correlated_idx] <- 1

# Inflate the effect for correlated events to have a mean of

correlated_non_focal_idx <-

setdiff(all_correlated_idx, focal_idx) # Fixing the selection of non-focal correlated events

data$ab_ret[correlated_non_focal_idx] <-

data$ab_ret[correlated_non_focal_idx] - mean(data$ab_ret[correlated_non_focal_idx]) + 1

# Define the numbers of uncorrelated events for each scenario

num_uncorrelated <- c(5, 10, 20, 30, 40)

# Define uncorrelated events

for (num in num_uncorrelated) {

for (i in 1:num) {

data[paste0("uncorrelated_", i)] <- 0

uncorrelated_idx <- sample(1:n, round(n * 0.1))

data[uncorrelated_idx, paste0("uncorrelated_", i)] <- 1

}

}

# Define uncorrelated columns and scenarios

unc_cols <- paste0("uncorrelated_", 1:num_uncorrelated)

results <- tibble(

Scenario = c(

"Include Correlated",

"Correlated Effects",

"Exclude Correlated",

"Exclude Correlated and All Uncorrelated"

),

MeanEffect = c(

mean_ci(data$ab_ret[data$focal == 1])$mean,

mean_ci(data$ab_ret[data$focal == 0 |

data$correlated == 1])$mean,

mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0])$mean,

mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0 &

rowSums(data[, paste0("uncorrelated_", 1:num_uncorrelated)]) == 0])$mean

),

LowerCI = c(

mean_ci(data$ab_ret[data$focal == 1])$lower,

mean_ci(data$ab_ret[data$focal == 0 |

data$correlated == 1])$lower,

mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0])$lower,

mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0 &

rowSums(data[, paste0("uncorrelated_", 1:num_uncorrelated)]) == 0])$lower

),

UpperCI = c(

mean_ci(data$ab_ret[data$focal == 1])$upper,

mean_ci(data$ab_ret[data$focal == 0 |

data$correlated == 1])$upper,

mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0])$upper,

mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0 &

rowSums(data[, paste0("uncorrelated_", 1:num_uncorrelated)]) == 0])$upper

)

)

# Add the scenarios for excluding 5, 10, 20, and 50 uncorrelated

for (num in num_uncorrelated) {

unc_cols <- paste0("uncorrelated_", 1:num)

results <- results %>%

add_row(

Scenario = paste("Exclude", num, "Uncorrelated"),

MeanEffect = mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0 &

rowSums(data[, unc_cols]) == 0])$mean,

LowerCI = mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0 &

rowSums(data[, unc_cols]) == 0])$lower,

UpperCI = mean_ci(data$ab_ret[data$focal == 1 &

data$correlated == 0 &

rowSums(data[, unc_cols]) == 0])$upper

)

}

ggplot(results,

aes(

x = factor(Scenario, levels = Scenario),

y = MeanEffect,

ymin = LowerCI,

ymax = UpperCI

)) +

geom_pointrange() +

coord_flip() +

ylab("Mean Effect") +

xlab("Scenario") +

ggtitle("Mean Effect of Focal Events under Different Scenarios") +

geom_hline(yintercept = true_effect,

linetype = "dashed",

color = "red")

Figure 39.2: Estimated mean focal-event effect with 95% confidence intervals across scenarios that include or exclude correlated and varying numbers of uncorrelated events. The dashed red line marks the true effect.

As shown in Figure 39.2, the inclusion of correlated events demonstrates minimal impact on the estimation of our focal events. Conversely, excluding these correlated events can diminish our statistical power. This is true in cases of pronounced correlation.

However, the consequences of excluding unrelated events are notably more significant. It becomes evident that by omitting around 40 unrelated events from our study, we lose the ability to accurately identify the true effects of the focal events. In reality and within research, we often rely on the Key Developments database, excluding over 150 events, a practice that can substantially impair our capacity to ascertain the authentic impact of the focal events.

This little experiment really drives home the point: you had better have a good reason to exclude an event from your study.

39.9 Biases in Event Studies

Event studies are subject to several biases that can affect the estimation of abnormal returns, the validity of test statistics, and the interpretation of results. The biases below are not exhaustive, and additional concerns specific to particular event types or markets may arise; the discussion focuses on the ones that recur often enough to warrant routine attention.

39.9.1 Timing Bias: Different Market Closing Times

When firms in the sample trade on exchanges in different time zones, the very notion of “the day of the event” becomes ambiguous. Campbell et al. (1998) flag this issue: a closing price recorded at 4 p.m. New York time and another at 4 p.m. Tokyo time correspond to substantially different information sets, and aggregating them as if they were contemporaneous obscures the true price reaction. The bias is especially acute for firms cross-listed on multiple exchanges or for events that release news during a specific time zone’s trading hours, after some markets have closed and before others open.

The standard fixes line up directly with the source of the problem. Use synchronized closing prices wherever possible, drawing on a single reference exchange or on intraday quotes recorded at a uniform timestamp. When that is not feasible, define the event window relative to the firm’s primary trading exchange and accept that the resulting estimate is conditional on that choice. In multi-exchange settings, reporting results separately by primary listing is a useful robustness exercise: substantial divergence is a flag that timing alignment is doing real work.

39.9.2 Intraday and High-Frequency Event Studies

The conventional event study works with daily returns because, until the early 2000s, daily was the finest granularity at which clean panel data on returns and corporate events was widely available. Two developments since then have made intraday and tick-level event studies a parallel methodological track rather than a niche variant: the standardisation of high-frequency exchange data (TAQ in the US, equivalent feeds elsewhere) and the routine timestamping of news events at the minute or second level in commercial data feeds (Bloomberg, Reuters, RavenPack, Capital IQ Key Developments). The payoff is that the event window contracts from days to minutes, which buys two things at once: dramatically lower contamination from coincident news, and the ability to identify the precise channel through which information enters prices.

The canonical reference is Andersen et al. (2003), who use five-minute exchange-rate returns sampled from high-frequency tick data to identify the price impact of macroeconomic announcements. Their key results, that announcement surprises induce conditional-mean jumps within minutes of release, that the price response is asymmetric in good versus bad news, and that volatility persists for hours after the announcement, established the template that subsequent intraday event studies have largely followed. In US equities, Lucca and Moench (2015) document a large equity excess return in the 24-hour window before scheduled FOMC announcements (measured from 2 p.m. the previous day to 2 p.m. the announcement day), the pre-FOMC drift, a result that is invisible at daily frequency because the close-to-close convention straddles the 2 p.m. announcement window. Boehmer et al. (2021) provide a method for tagging marketable retail trades in TAQ data and pair it with high-frequency event studies of retail-driven news, opening a separate channel for asking who actually trades on which information.

A second class of high-frequency studies attacks the signal extraction problem rather than the timing problem. Boudoukh et al. (2019) use textual analysis of firm-specific news to identify the news content underlying price moves and to separate news-driven moves from microstructural noise, finding that identified news accounts for roughly half of overnight idiosyncratic return variance. The methodology generalises directly to firm-specific event studies in samples where multiple news items can arrive on the same day: instead of dropping contaminated firm-days, the analyst attributes the price move to the textually identified news content and proceeds. This approach is increasingly the norm in studies that need to disentangle the contribution of overlapping announcements, regulatory disclosures, earnings, M&A news, and analyst reports.

Three practical guidelines follow from the intraday literature. First, when the event has a precise public timestamp (a press-release time, a regulatory filing timestamp, an exchange-disseminated news flag), shrink the event window to the smallest interval that contains the news. The price reaction is concentrated in the minutes around the announcement, and wider windows mostly add noise. Second, when multiple events plausibly arrive on the same day, textual attribution via NLP is the most defensible way to isolate the focal event’s contribution. Third, the standard parametric tests carry over to intraday data with the obvious caveat that intraday return distributions are heavier-tailed than daily ones, so the BMP and Kolari-Pynnonen adjustments (Section 39.6.2.4 and Section 39.6.2.5) and the nonparametric GRANK test are all the more important.

39.9.3 Upward Bias in Cumulative Abnormal Returns

A subtler bias arises in the aggregation of daily abnormal returns into cumulative returns. The mechanism is microstructural rather than statistical: transaction prices recorded at the bid or the ask, rather than at the midpoint, introduce small jumps that the abnormal-return calculation reads as price movement. Liquidity constraints amplify the effect, because thinly traded stocks tend to bounce between bid and ask prices in patterns that look like genuine return innovations. When these microstructural jumps are aggregated over a multi-day event window, the cumulative abnormal return inherits a small but systematic upward bias.

The fixes operate either at the input or at the inference stage. At the input stage, replace raw transaction prices with volume-weighted average prices (VWAP) or with bid-ask midpoints, both of which average out the microstructural noise. At the inference stage, apply heteroskedasticity-robust or microstructure-corrected standard errors, which keep the point estimate unchanged but widen the confidence interval to reflect the additional variance introduced by the bias. For events with very short windows (single trading day), the input-stage fix is more important; for longer windows where the noise averages out anyway, the inference-stage fix usually suffices.

39.9.4 Cross-Sectional Dependence Bias

Cross-sectional dependence in returns biases standard-deviation estimates downward, which in turn inflates test statistics whenever multiple firms experience the event on the same date. MacKinlay (1997) flagged the issue early on, noting that the problem becomes acute when firms in the same industry or market share event dates and so face common shocks that the independence assumption simply cannot accommodate. Wiles et al. (2012) document the consequences empirically: in concentrated industries, the dependence is severe enough to materially inflate test statistics, and the apparent significance of an event can dissolve once the correction is applied.

Two corrections are standard in the literature, and they target the bias from different angles. The Calendar-Time Portfolio Abnormal Returns (CTAR) approach (Jaffe 1974) reorganizes the data into calendar-time portfolios so that all firms experiencing the event on the same day enter as a single portfolio observation rather than as multiple correlated observations. The dependence problem disappears by construction because there is no longer cross-firm variation within a portfolio. The time-series standard-error correction of Brown and Warner (1980) takes the opposite route: keep the firm-level structure but estimate the variance from the time-series of the cross-sectional aggregate, capturing the dependence in the variance estimate rather than averaging it away. Both approaches are well-tested in the literature; the choice between them often comes down to whether the analyst wants firm-level attribution (Brown-Warner) or pooled portfolio-level inference (Jaffe).

# Load required libraries

library(sandwich) # For robust standard errors

library(lmtest) # For hypothesis testing

# Simulated dataset

set.seed(123)

df_returns <- data.frame(

event_id = rep(1:100, each = 10),

firm_id = rep(1:10, times = 100),

abnormal_return = rnorm(1000, mean = 0.02, sd = 0.05)

)

# Cross-sectional dependence adjustment using clustered standard errors

model <- lm(abnormal_return ~ 1, data = df_returns)

coeftest(model, vcov = vcovCL(model, cluster = ~event_id))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.0208064 0.0014914 13.951 < 2.2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 139.9.5 Sample Selection Bias

Event studies often suffer from self-selection bias because firms choose to undertake the events they undertake (issuing equity, announcing an acquisition, recalling a product) on the basis of private information that the analyst does not observe. The firm’s choice is, in effect, a treatment-assignment mechanism that depends on unobservables, and the resulting comparison between event firms and non-event firms reads partly as a treatment effect and partly as the difference in the unobservables that drove the decision. This is the canonical omitted-variable bias problem, with the omitted variable being whatever private information the firm acted on.

39.9.6 Corrections for Sample Selection Bias

Several corrections are available, and the right one depends on the institutional details of the event and on what auxiliary information is available.

The Heckman two-stage model (Acharya 1993) is the parametric approach. A first-stage probit predicts the probability of experiencing the event from observable firm characteristics, and the resulting inverse-Mills ratio enters the second-stage regression of abnormal returns as a control for the unobserved selection mechanism. The strength of the approach is that it has a clear identification logic and a familiar implementation; the weakness is that it requires an exclusion restriction, a variable that affects the probability of the event but not the abnormal return directly, and such instruments are notoriously hard to find in event-study settings.

Counterfactual-observation methods are the non-parametric alternative. Two are common in event-study work. Propensity-score matching pairs each event firm with a non-event firm that has similar observable characteristics, on the logic that conditional on observables the event is as good as random. Switching regression explicitly models the two regimes (event vs. no event) jointly with the selection mechanism, allowing for unobserved heterogeneity in the relationship between firm characteristics and outcomes across the two regimes. Both are useful when the available observables are rich enough to capture the bulk of the selection process.

The remainder of this section walks through each correction in turn, with a code example for the Heckman and propensity-score-matching cases.

- Heckman Selection Model

A Heckman selection model can be used when private information influences both event participation and abnormal returns.

Examples: Y. Chen et al. (2009); Wiles et al. (2012); Fang et al. (2015)

Steps:

First Stage (Selection Equation): Model the firm’s probability of experiencing the event using a Probit regression.

Second Stage (Outcome Equation): Model abnormal returns, controlling for the estimated Mills ratio (\(\lambda\)).

# Load required libraries

library(sampleSelection)

# Simulated dataset for Heckman model

set.seed(123)

df_heckman <- data.frame(

firm_id = 1:500,

event = rbinom(500, 1, 0.3), # Event occurrence (selection)

firm_size = runif(500, 1, 10), # Firm characteristic

abnormal_return = rnorm(500, mean = 0.02, sd = 0.05)

)

# Introduce selection bias by correlating firm_size with event occurrence

df_heckman$event[df_heckman$firm_size > 7] <- 1

# Heckman Selection Model

heckman_model <- selection(

selection = event ~ firm_size, # Selection equation

outcome = abnormal_return ~ firm_size, # Outcome equation

data = df_heckman

)

# Summary of Heckman model

summary(heckman_model)

#> --------------------------------------------

#> Tobit 2 model (sample selection model)

#> Maximum Likelihood estimation

#> Newton-Raphson maximisation, 6 iterations

#> Return code 8: successive function values within relative tolerance limit (reltol)

#> Log-Likelihood: 165.4579

#> 500 observations (239 censored and 261 observed)

#> 6 free parameters (df = 494)

#> Probit selection equation:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -1.75936 0.15793 -11.14 <2e-16 ***

#> firm_size 0.33933 0.02776 12.22 <2e-16 ***

#> Outcome equation:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.006025 0.040359 0.149 0.881

#> firm_size 0.001311 0.004205 0.312 0.755

#> Error terms:

#> Estimate Std. Error t value Pr(>|t|)

#> sigma 0.049048 0.002836 17.297 <2e-16 ***

#> rho 0.188195 0.421944 0.446 0.656

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------Interpretation

If the Mills ratio (\(\lambda\)) is significant, it indicates that private information affects CARs.

Weak instruments can lead to multicollinearity, making the second-stage estimates unreliable.

- Propensity Score Matching

PSM matches event firms with similar non-event firms, controlling for selection bias.

Examples of PSM in Finance and Marketing:

# Load required libraries

library(MatchIt)

# Simulated dataset

set.seed(123)

df_psm <- data.frame(

firm_id = 1:1000,

event = rbinom(1000, 1, 0.5), # 50% of firms experience an event

firm_size = runif(1000, 1, 10),

market_cap = runif(1000, 100, 10000)

)

# Propensity score matching (PSM)

match_model <- matchit(event ~ firm_size + market_cap, data = df_psm, method = "nearest")

# Summary of matched sample

summary(match_model)

#>

#> Call:

#> matchit(formula = event ~ firm_size + market_cap, data = df_psm,

#> method = "nearest")

#>

#> Summary of Balance for All Data:

#> Means Treated Means Control Std. Mean Diff. Var. Ratio eCDF Mean

#> distance 0.4987 0.4875 0.2093 1.0656 0.0602

#> firm_size 5.2627 5.6998 -0.1683 1.0530 0.0494

#> market_cap 5208.5283 4868.5828 0.1163 1.0483 0.0359

#> eCDF Max

#> distance 0.1152

#> firm_size 0.0902

#> market_cap 0.0713

#>

#> Summary of Balance for Matched Data:

#> Means Treated Means Control Std. Mean Diff. Var. Ratio eCDF Mean

#> distance 0.4987 0.4898 0.1668 1.1170 0.0489

#> firm_size 5.2627 5.6182 -0.1369 1.0693 0.0404

#> market_cap 5208.5283 4949.8521 0.0885 1.0594 0.0283

#> eCDF Max Std. Pair Dist.

#> distance 0.1034 0.1673

#> firm_size 0.0872 0.6549

#> market_cap 0.0649 0.9168

#>

#> Sample Sizes:

#> Control Treated

#> All 507 493

#> Matched 493 493

#> Unmatched 14 0

#> Discarded 0 0

# Extract matched data

matched_data <- match.data(match_model)Advantages of PSM

Controls for observable differences between event and non-event firms.

Reduces selection bias while maintaining a valid control group.

- Switching Regression

A Switching Regression Model accounts for selection on unobservables using instrumental variables.

- Example: Cao and Sorescu (2013) applied switching regression to compare two outcomes while correcting for selection bias.

39.10 Does CAR Measure Value Creation? Evidence from M&A

The discussion so far has treated the cumulative abnormal return as a well-defined object: under the four assumptions in Section 39.2, CAR is the market’s revaluation of the firm in light of the event’s information content. A separate and harder question is whether that revaluation actually tracks the ex-post value created by the event. The two are not the same. CAR measures what investors believed about the event at the moment the news broke; ex-post value is what the event actually produced over the subsequent months and years. A growing body of work shows that the gap between the two can be large, persistent, and in places systematic. The cleanest setting in which to see this is corporate mergers and acquisitions, where the event is precisely dated, the dollar stakes are enormous, and ex-post outcomes (operating performance, productivity, divestitures, write-downs) are observable.

39.10.1 The M&A Stylized Facts

The textbook short-window finding is by now well-rehearsed. Bradley et al. (1988) showed that the combined CAR of target and acquirer, the synergy gain, is reliably positive around tender-offer announcements, around 7.4 percent of combined market capitalization on average. The split between target and acquirer is lopsided: targets routinely earn 20 to 30 percent abnormal returns around mergers and 30 to 40 percent around tender-offer premia, while acquirers earn close to zero on average. Andrade et al. (2001) synthesized two decades of this evidence and concluded that mergers create value, but that the acquirer’s share is small and often negative. The standard inference was that markets price the deal efficiently, the gains accrue to targets because of competitive bidding, and the average acquirer is paying close to fair value.

That inference began to fray in the early 2000s. Moeller et al. (2004) document a strong size effect: large acquirers earn significantly negative announcement returns, even as small acquirers earn positive ones. Moeller et al. (2005) quantify the aggregate consequence: acquirers lost on the order of 240 billion dollars at announcement during the 1998 to 2001 merger wave alone, an order of magnitude larger than any plausible synergy estimate. Bhagat et al. (2005) propose probability-scaled CARs and methods that exploit returns at intervening events to back out the surprise component of the announcement, and conclude that the perceived value improvements from tender offers are larger than raw CAR suggests, that is, that raw CAR understates value creation. Bouwman et al. (2009) show that announcement returns vary systematically with the market valuation environment in which the deal is launched, with high-valuation acquisitions earning high short-run CAR but underperforming over the long run. Bargeron et al. (2008) decompose the public-versus-private acquirer gap and link it to differences in bidder managerial ownership, a channel that announcement-window CAR cannot reveal. Cai and Sevilir (2012) and Harford et al. (2012) tie negative acquirer CAR to specific governance failures, board interlocks in the first case, managerial entrenchment in the second.

Two strands of evidence push directly against the CAR-as-value-creation interpretation. The long-run shareholder benefit literature, anchored by Loughran and Ritter (1997), documents large negative five-year buy-and-hold abnormal returns for stock-merger acquirers (around minus 25 percent over five years in their sample) alongside positive five-year returns for cash-tender-offer acquirers, a divergence that is entirely invisible in the announcement window. The operating-performance and restructuring literature anchors at Healy et al. (1992), who use accounting cash-flow data on the 50 largest US mergers from 1979 through mid-1984 to document post-merger operating-performance gains, and extends through Maksimovic and Phillips (2001) and Maksimovic et al. (2011), who use Census plant-level data to show that acquirers extensively reorganize target assets in the years after the deal, selling roughly 27 percent of target plants and closing another 19 percent within three years. Whatever value mergers ultimately create or destroy is realized through this restructuring, not through the announcement-window price move. Maksimovic et al. (2013) extend the comparison to public versus private acquirer waves and find that the two sets of acquirers differ systematically in the magnitude of productivity gains they generate, with public-firm acquirers realizing larger gains on-the-wave and when their stock is highly valued. Golubov et al. (2015) close the loop by showing that acquirer announcement returns are persistent at the firm level, the same acquirers earn unusually high or low CAR across multiple deals, suggesting that CAR reflects an acquirer-specific characteristic that travels with the firm rather than a deal-specific assessment.

39.10.2 The (Missing) Relation

Ben-David et al. (2026) put this body of evidence on a sharper footing. They take as their premise the workhorse interpretation, that the acquirer’s announcement-period CAR is the market’s expectation of the value the deal will create, and ask the obvious question: does CAR correlate with ex-post outcomes? They construct a battery of value-creation measures using post-deal data: changes in operating performance, write-downs and impairments of acquired goodwill, divestitures of acquired assets, and the long-horizon survival of the combined entity. They then show, across a large sample of US acquisitions, that announcement CAR is essentially uncorrelated with each of these ex-post outcomes. The (Missing) Relation between Acquisition Announcement Returns and Value Creation is not a statistical artifact of a particular benchmark or window, the result survives a wide range of factor-model and characteristic-benchmark choices and a wide range of event-window definitions.

Two of their secondary results matter for how to read the broader literature. First, a simple characteristics-based model using only information publicly available at announcement time predicts ex-post outcomes reasonably well, that is, the missing relation is not because outcomes are intrinsically unpredictable. Second, decomposing CAR into a component driven by acquirer characteristics and a component driven by deal characteristics shows that the acquirer-specific component dominates: announcement-period CAR is mostly news about the standalone acquirer that happens to arrive on the deal date, not news about the deal itself. This rationalises the Golubov et al. (2015) persistence finding and explains why CAR fails as a deal-quality signal in the first place: it is mostly not measuring the deal.

39.10.3 A Replication on Public Data

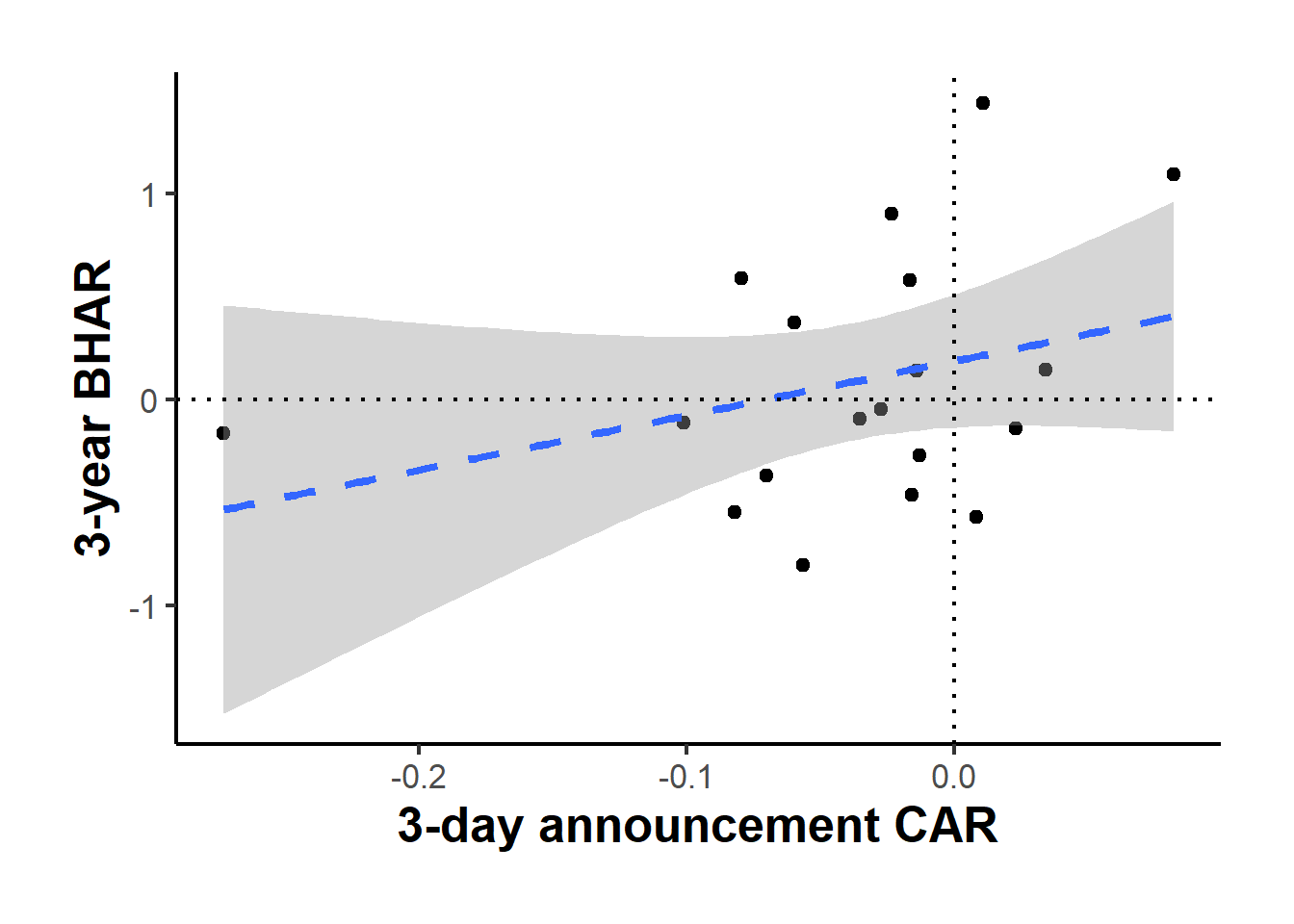

Ben-David et al. (2026) work from a large proprietary panel of deals matched to SDC Platinum and Compustat, which is not reproducible without a WRDS subscription. Under the Journal of Finance’s Data and Code Sharing Policy, the authors’ code is deposited alongside the published article, but the underlying SDC, CRSP, and Compustat inputs remain restricted to WRDS subscribers, so the official package documents rather than removes this barrier. What is reproducible with nothing more than free daily stock prices is the closely related question that motivates the Loughran-Ritter strand of the literature discussed above: does the market’s announcement-window verdict on a deal (CAR) line up with what happened to the acquirer’s stock over the following three years (BHAR)? The two measures are not identical to the operating-performance and impairment measures in Ben-David et al. (2026), a price-based long-run return is itself a noisy, discount-rate-contaminated object, but the exercise is a direct, from-scratch test of the same underlying claim: that a short announcement window is a poor guide to how a deal actually turns out.

The replication uses nineteen large, well-documented US acquisitions announced between 2005 and 2018, chosen because each acquirer traded under a single unchanged ticker for years before and after the deal, which keeps the exercise a plain market-model calculation with no ticker-splicing. The list deliberately spans both deals with a reputation for destroying value (HP/Autonomy, eBay/Skype, Bank of America/Countrywide) and deals with a reputation for creating it (Disney/Pixar, Disney/Marvel, Amazon/Whole Foods), so the sample is not selected on the outcome being tested.

library(tidyverse)

deals <- read.csv("data/car_bhar_replication.csv") %>%

mutate(date = as.Date(date), announce_date = as.Date(announce_date))

# One row per firm-day: rel_day = 0 is the announcement's first trading day

# (Disney/Lucasfilm uses Oct 31, 2012, the first day markets reopened after

# Hurricane Sandy closed the NYSE on the announcement date itself).

c(n_deals = n_distinct(deals$deal), n_firm_days = nrow(deals))

#> n_deals n_firm_days

#> 19 19779For each deal the estimation window is trading days -260 to -31 relative to the announcement, exactly the market-model setup from Step 2 and Step 3 of Section 39. CAR is the sum of market-model abnormal returns over the three-day window (-1, +1). BHAR is the buy-and-hold abnormal return, computed with the same product formula as Section 39.11.1, from two trading days after the announcement out to roughly three years later (trading day +761), against SPY as the benchmark in both stages.

compute_deal <- function(sub) {

est <- filter(sub, rel_day >= -260, rel_day <= -31)

ev <- filter(sub, rel_day >= -1, rel_day <= 1)

lr <- filter(sub, rel_day >= 2, rel_day <= 761)

mm <- lm(ret_stock ~ ret_mkt, data = est)

ar_event <- ev$ret_stock - predict(mm, newdata = ev)

car <- sum(ar_event)

stock_gross <- prod(1 + (exp(lr$ret_stock) - 1))

mkt_gross <- prod(1 + (exp(lr$ret_mkt) - 1))

bhar <- stock_gross - mkt_gross

tibble(CAR = car, BHAR = bhar, beta = coef(mm)[["ret_mkt"]])

}

results <- deals %>%

group_by(deal) %>%

group_modify(~ compute_deal(.x)) %>%

ungroup() %>%

arrange(desc(CAR))| deal | 3-day CAR | 3-year BHAR | Market beta |

|---|---|---|---|

| Comcast / NBCUniversal | 0.082 | 1.090 | 1.183 |

| Disney / 21st Century Fox | 0.034 | 0.145 | 0.619 |

| Berkshire Hathaway / BNSF | 0.023 | -0.139 | 0.801 |

| Amazon / Whole Foods | 0.011 | 1.437 | 1.012 |

| Bank of America / Countrywide | 0.008 | -0.570 | 1.057 |

| Verizon / Yahoo | -0.013 | -0.269 | 0.702 |

| Disney / Pixar | -0.014 | 0.141 | 0.882 |

| eBay / Skype | -0.016 | -0.462 | 1.110 |

| Disney / Marvel | -0.017 | 0.576 | 1.100 |

| Disney / Lucasfilm | -0.023 | 0.900 | 1.111 |

| AT&T / DirecTV | -0.027 | -0.048 | 0.755 |

| Merck / Schering-Plough | -0.035 | -0.093 | 0.822 |

| Bank of America / Merrill Lynch | -0.057 | -0.802 | 1.966 |

| Google / Motorola Mobility | -0.060 | 0.373 | 1.029 |

| CVS Health / Aetna | -0.070 | -0.367 | 0.667 |

| Microsoft / Nokia D&S | -0.080 | 0.588 | 0.926 |

| IBM / Red Hat | -0.082 | -0.548 | 0.960 |

| Pfizer / Wyeth | -0.101 | -0.112 | 0.777 |

| HP / Autonomy | -0.273 | -0.163 | 0.762 |

HP/Autonomy shows the most extreme announcement reaction, a -27 percent three-day CAR, but that number is not a clean read on the Autonomy deal at all: HP bundled the acquisition announcement with news that it was considering spinning off its PC business and killing the webOS TouchPad on the same day, August 18, 2011, so the announcement window absorbed three pieces of firm-specific news at once. It is the muddiest event in the sample, exactly the case the Implications for Practice discussion below warns about, and it happens to be the deal later confirmed, via an $8.8 billion goodwill impairment and a UK High Court fraud finding against Autonomy’s founder, to have destroyed the most value.

ggplot(results, aes(CAR, BHAR)) +

geom_point(size = 2) +

geom_smooth(method = "lm", se = TRUE, linetype = "dashed") +

geom_hline(yintercept = 0, linetype = "dotted") +

geom_vline(xintercept = 0, linetype = "dotted") +

labs(x = "3-day announcement CAR", y = "3-year BHAR") +

causalverse::ama_theme()

Figure 39.3: Three-day announcement CAR against three-year buy-and-hold abnormal return for nineteen large US acquisitions. The dashed line is the OLS fit; a flat or noisy relationship is what the missing-relation result predicts.

#> Pearson correlation: 0.32 (95% CI -0.16 to 0.67, p = 0.18, n = 19)The correlation is positive but small, imprecisely estimated, and not distinguishable from zero at conventional levels with a sample this size. That is the point: even on a hand-picked set of highly visible deals with three-day CARs ranging from minus 27 percent to plus 8 percent, the announcement’s verdict does not reliably forecast where the stock stands three years later. Disney’s four acquisitions in the table make the case in miniature. Pixar and Marvel earned negative announcement CAR (the market’s initial reaction was that Disney overpaid) but went on to strong positive three-year BHAR, while Lucasfilm’s announcement CAR was the most negative of the four and its long-run BHAR the most positive, the opposite of what a CAR-as-value-creation reading would predict. This is a small, non-random, US-only, price-based replication, not a substitute for the accounting-based panel in Ben-David et al. (2026), but it reproduces the qualitative result with nothing more than free data and a market model: the announcement window and the long run are, empirically, close to unrelated objects. A natural extension is to pull a larger sample from CRSP and SDC Platinum, add the impairment- and divestiture-based outcomes from Compustat that Ben-David et al. (2026) and Masulis et al. (2023) use, and check whether the weak correlation survives the larger, unselected sample, exactly the robustness check the chapter’s Sample in Event Studies guidance recommends before generalising from a small hand-picked set of deals.

39.10.4 Implications for Practice

The Ben-David et al. result does not invalidate event studies, but it sharply constrains what claims they can support. Three implications are worth flagging.

First, for M&A specifically, announcement CAR is a poor proxy for expected value creation. Treating it as one, for example by using it as the dependent variable in a cross-sectional regression of “what deal characteristics create value”, is essentially regressing on an outcome whose signal-to-noise ratio for the deal is close to zero. Modern best practice in M&A empirics increasingly pairs CAR with ex-post measures, operating-performance changes (Healy et al. 1992), productivity gains (Maksimovic and Phillips 2001; Maksimovic et al. 2011), impairment- and divestiture-based outcomes (Ben-David et al. 2026), or asset-level decompositions of where the gains actually originate (Masulis et al. 2023, who trace acquirer value creation in intangible-asset deals to the target’s pre-deal innovation efficiency and the acquirer’s post-deal ability to redeploy the acquired intangibles), and treats agreement between the two as the substantive finding.

Second, the result generalises to event studies in any setting where the focal event arrives bundled with substantial firm-specific information. Earnings announcements, regulatory rulings affecting a single firm, and major product launches all share the structural feature that the announcement-window CAR is dominated by news about the firm that happens to arrive on the event date. The cleaner the event (a regulatory decision affecting many firms simultaneously, a court ruling with timing exogenous to the firm), the closer CAR comes to measuring the event’s effect; the muddier the event (a strategic firm choice with substantial coincident firm-specific news), the more the warning applies.